(Image credit: Getty Images)

For decades, the 401(k) was hailed as the cornerstone of the American retirement dream. However, a quiet revolution has taken place, resulting in a monumental shift in the U.S. retirement landscape: assets in traditional individual retirement accounts (IRAs) now exceed those in 401(k) plans by approximately $9.1 trillion.

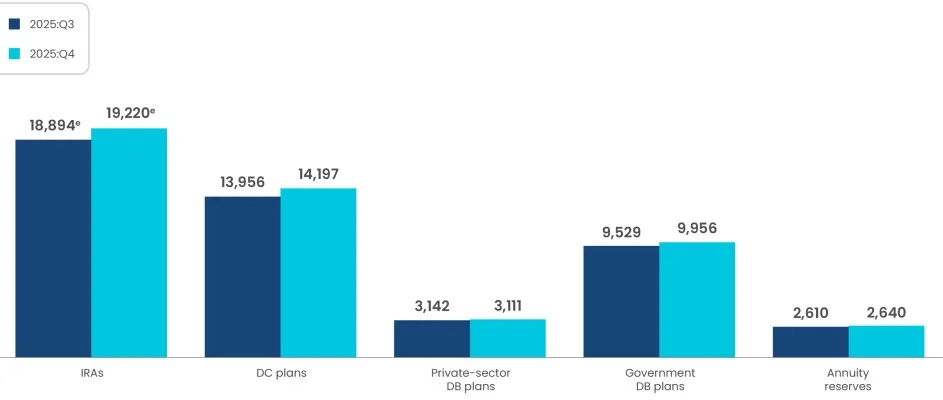

As of Q4 of 2025, employees held $10.1 trillion in employer-sponsored 401(k)s and $19.2 trillion in IRAs, according to the Investment Company Institute. This massive migration of wealth, fueled by a lifetime of job changes and rollovers, has fundamentally altered the safety net for millions. While IRAs offer unparalleled freedom, they also strip away the institutional ‘guardrails’ that once protected savers from high fees, legal risks and their own worst impulses.

It’s an issue that impacts more than half of traditional IRA owners. By mid-2024, 59% of traditional IRA–owning households indicated that their traditional IRAs held rollovers from employer-sponsored retirement plans.

Sign up for Kiplinger’s Free Newsletters

Profit and prosper with the best of expert advice on investing, taxes, retirement, personal finance and more – straight to your e-mail.

Profit and prosper with the best of expert advice – straight to your e-mail.

Retirement Assets by Type- billions of dollars, end-of-period, 2025: Q3 – 2025: Q4

(Image credit: Investment Company Institute. Americans held $14.2 trillion in all employer-based DC retirement plans on December 31, 2025, of which $10.1 trillion was held in 401(k) plans.)

“This massive migration of wealth, fueled by a lifetime of job changes and rollovers, has fundamentally altered the safety net for millions.”

Rollovers and retirement saving

(Image credit: Getty Images)

The primary driver of this shift is rollovers. While 401(k) plans are the primary vehicle for active workers to save, many people roll their balances into traditional IRAs when they change jobs or retire. Over decades, this has moved trillions of dollars out of employer-sponsored plans and into the retail IRA market. Rollovers are projected to grow to over $1 trillion in 2030 from $907 billion in 2026.

The Investment Company Institute’s (ICI) latest research shows that as of mid-2024, 44% of US households owned IRAs. And, traditional IRAs were the most common type of IRA owned. A whopping 59% of traditional IRA-owning households indicated that their traditional IRAs contained rollovers from employer-sponsored retirement plans; 85% had rolled over the entire retirement account balance in their most recent rollover.

This movement of money from 401(k)s to IRAs leaves workers more vulnerable because IRAs lack the protections provided by the Employee Retirement Income Security Act of 1974, or ERISA.

Roth and traditional IRA balances are exempted from the bankruptcy estate up to $1,711,975 under the Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 (BAPCPA). The $1,711,975 does not include funds rolled into the IRA. Former employer plan dollars remain 100% protected from bankruptcy within the IRA and do not reduce the cap. However, in non-bankruptcy situations, state laws apply to IRA assets, including rollover IRAs.

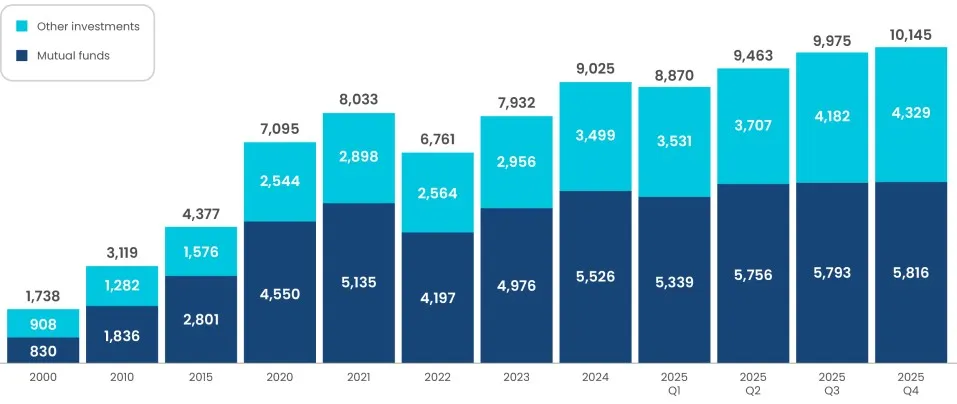

401(k) Plan Assets- billions of dollars, end-of-period, selected periods

(Image credit: Note: Components may not add to the total because of rounding. Sources: Investment Company Institute and Department of Labor)

Risks intrinsic to rolling over a federally-protected 401(k) into an IRA include:

- Lower fiduciary standards: 401(k) plans are strictly governed by ERISA, which requires plan sponsors to act as fiduciaries — the highest legal standard of care. In contrast, the standards for broker-dealers selling IRA investments are often less protective, potentially leading to suboptimal investment choices that benefit the provider more than the saver.

- Increased “leakage”: 401(k)s are designed to keep money locked away until retirement; withdrawals are generally only permitted for specific hardships or as rollovers after a job change. IRAs allow withdrawals at any time for any reason and have more tax-favored exceptions, making it easier to deplete their accounts.

- Weakened creditor protections: Assets in 401(k) plans are robustly protected from bankruptcy and legal judgments. IRA protections are not as comprehensive and vary significantly by state, leaving these assets more exposed to creditors.

- Higher fees and less transparency: ERISA mandates clear, understandable fee disclosures for 401(k)s. IRAs often have more complex fee structures and less transparency.

- Spousal protections: With a 401(k), a spouse is the default beneficiary by law and must sign a notarized waiver for the participant to name someone else. IRAs have no such federal requirement, allowing owners to change beneficiaries without their spouse’s knowledge or consent.

Job mobility and retirement savings

(Image credit: Getty Images)

Gone are the days when you worked at one job the majority of your adulthood and retired with a pension and a gold watch. While late baby boomers and Gen Xers were 401(k) pioneers, millennials and Gen Z are natives of the gig economy. The average American worker changes jobs 12 times over their career. Having more than one employer before you retire is expected and a reality of the modern economy.

“Active retirement management is more important than ever,” Romi Savova, founder and CEO of PensionBee, told Kiplinger. “In many cases, it can be helpful to find an IRA home. Having a trusted destination for your 401(k)s makes sense, as you may need to roll over more than once throughout your career. 401(k) rollovers are notoriously difficult, so ensure you are working with a provider that offers hands-on support.”

Traditional IRA-owning households with rollovers cite three main reasons for rolling over their retirement plan assets into traditional IRAs: not wanting to leave assets behind at the former employer (23%), wanting to consolidate assets (19%), and wanting more investment options (14%), according to the ICI.

Approximately 14.8 million defined-contribution plan participants change jobs each year, per the Employee Benefit Research Institute. Over 6 million of these participants have less than $7,000 in their accounts when they change jobs, and are subject to a mandatory distribution from their former retirement plan into a Safe Harbor IRA. Over 75% of these accounts will cash out by year seven. This is an example of ‘leakage’ — the early withdrawal of retirement funds that erodes long-term growth.

Another important aspect of having multiple jobs and, by extension, multiple retirement accounts, is the loss of momentum. A hidden danger in switching jobs is the reduction in retirement plan contributions. The median job switcher saw a 10% increase in pay, but a 0.7% decline in their retirement saving rate when they switched employers, according to Vanguard.

Five ways to protect your money in an IRA

(Image credit: Getty Images)

While IRAs offer more flexibility and investment choices, the loss of institutional oversight and legal protection can’t be ignored or left unaddressed. “IRAs can be acquired from a variety of different institutions, including banks, wealth management companies, and financial technology companies,” Savova said.

She notes that although many advisors can assist with the transition, it’s important to pick one who operates under a strict fiduciary mandate.

Although IRAs lack the same fiduciary guardrails and legal shields as employer-sponsored plans, that doesn’t mean you don’t have options for protecting your money. However, that does mean you’ll need to be more proactive and disciplined about protecting it than if you had a plan administrator and a raft of regulations that come with an employer-sponsored retirement plan.

While the Biden administration sought to extend ERISA fiduciary status to securities brokers and insurance agents, the rule was halted by court challenges and stay orders. The Trump administration ultimately declined to defend the policy, leading the Employee Benefits Security Administration (EBSA) to issue a formal vacatur notice invalidating the rule.

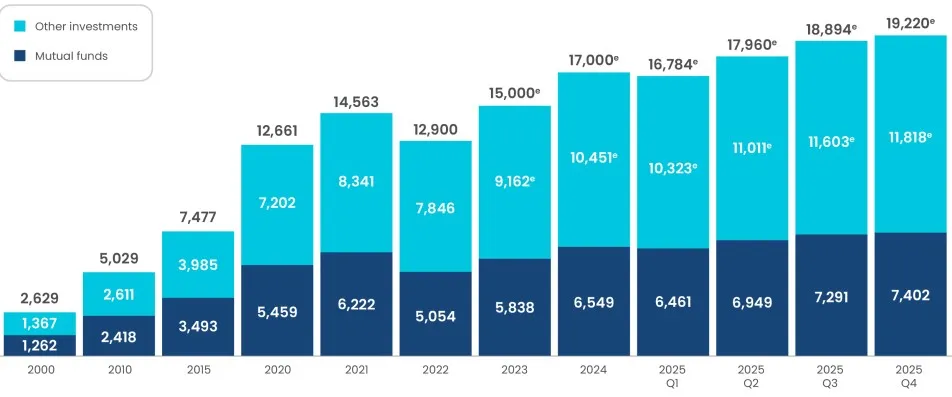

IRA Market Assets- billions of dollars, end-of-period, selected periods

(Image credit: Data marked “e” are estimated. Note: Components may not add to the total because of rounding. Sources: Investment Company Institute, Federal Reserve Board, American Council of Life Insurers, and Internal Revenue Service Statistics of Income Division)

Here are five ways to protect your money in an IRA:

1. Work with a fiduciary advisor

IRA providers (often broker-dealers) are not always held to the same high fiduciary standards as 401(k) plan sponsors. To mimic the protection of a 401(k), ensure that any financial professional you work with is a Certified Financial Planner (CFP) or a Registered Investment Advisor (RIA) who is legally obligated to act in your best interest.

2. Implement self-imposed “leakage” barriers

IRAs make it easier to withdraw money than 401(k)s do, often leading to “leakages” that deplete retirement savings. To protect your future balance:

- Automate your mindset: Treat the IRA as “untouchable” by not linking it directly to your primary checking account for easy transfers.

- Avoid the “exceptions”: While IRAs allow penalty-free withdrawals for things like first-time home purchases or education, using these can severely derail your compound interest.

3. Review and update beneficiary designations

In a 401(k), the law automatically designates a spouse as the beneficiary unless they sign a waiver. IRAs do not have this federal requirement. To protect your family’s inheritance, you must manually ensure your beneficiary forms are up to date. This is especially important after major life events like marriage, divorce or the birth of a child.

4. Understand your state’s creditor protections

IRAs generally offer less protection than 401(k)s in the event of litigation or bankruptcy. While 401(k)s have broad federal protection under ERISA, IRA protection often varies by state.

Research your state laws regarding IRA exemptions from creditors. If you live in a state with weak protections, you may want to consider additional liability insurance (like an umbrella policy) to protect your assets from potential lawsuits.

5. Scrutinize Fees and Disclosures

Because IRAs lack the standardized fee disclosure requirements of 401(k)s, high administrative costs and investment fees can silently eat away at your savings. “Many providers hide their fees through ‘zero-fee’ claims, but a closer look may reveal hidden transaction costs and investment costs. The average 401(k) cost ranges from 0.3% to 1.3%, so ensure your IRA fees are within an appropriate and similar range,” said Savova.

- Compare expense ratios: Look for low-cost index funds or ETFs within your IRA.

- Check for hidden costs: Be wary of 12b-1 fees or high commissions on products like annuities or actively managed funds that a broker might recommend.

Vigilance is your friend

(Image credit: Getty Images)

The shift toward IRAs is likely irreversible, but the vulnerability it creates doesn’t have to be. By understanding the guardrails that disappear when leaving a 401(k), savers can take deliberate steps to rebuild them.

“Former employers can charge additional fees for left-behind accounts and, in some cases, move assets to a new provider without your knowledge or consent,” cautioned Savova of Pension Bee. That’s why you need to be an active participant in planning your retirement.

“Rollovers are now an established part of the retirement saving process, so IRAs and 401(k)s should really be thought of as complementary accounts,” she said. “They are both established tools for navigating a fragmented system, and both support wealth building in different ways.”

Whether it is seeking out true fiduciary advice, self-regulating early withdrawals, or checking state-specific creditor laws, the burden of protection has moved from the employer to the individual. In this new era of retirement, being a “wise saver” is no longer enough; one must also become a vigilant protector of one’s own legacy.