(Image credit: Getty Images)

The Senate is on track to confirm Kevin Warsh to succeed Jerome Powell as Fed chair by Friday, May 15. That’s when Powell’s term as Fed chair is scheduled to expire. And President Donald Trump would like Warsh to cut interest rates as soon as June 16-17, at the next Fed meeting.

But decisions about the federal funds rate are made by a committee. And the Fed chair is just one of 12 voting members of the Federal Open Market Committee. The FOMC includes the seven members of the board, the president of the Federal Reserve Bank of New York, and four other regional Fed bank presidents who serve one-year rotating terms.

Powell’s term as a member of the Federal Reserve Board of Governors doesn’t expire until January 31, 2028. And he’s said he won’t leave until an investigation of the central bank for cost overruns on a renovation project is “well and truly over, with transparency and finality” and will do what he thinks “is best for the institution and the people we serve.”

Sign up for Kiplinger’s Free Newsletters

Profit and prosper with the best of expert advice on investing, taxes, retirement, personal finance and more – straight to your e-mail.

Profit and prosper with the best of expert advice – straight to your e-mail.

As much as Powell’s presence complicates the politics, any plans to cut (or raise!) the fed funds rate must gain the support of at least seven voting members of the FOMC. The Fed chair doesn’t even have tie-breaking power.

Cutting interest rates is one thing he can’t do right now or ever all by himself. But there are three things Kevin Warsh can do to change the Fed over the length of his initial four-year term.

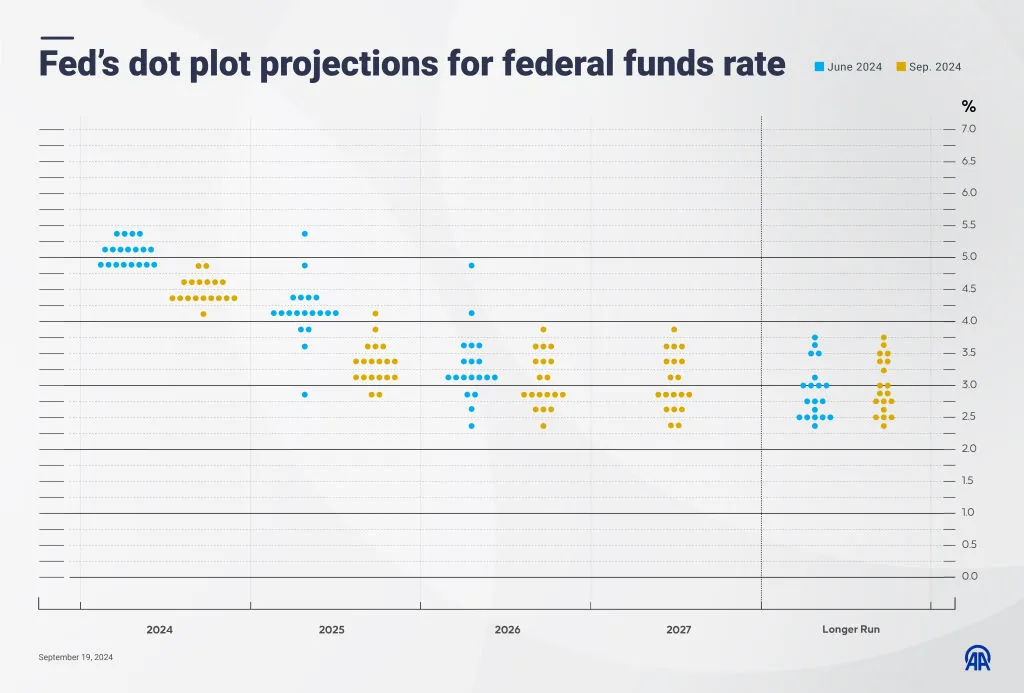

The plot against the dot plot

Markets have grown accustomed to celebrity Fed chairs and the “transparency” they seem to support. They and their fellow members of the board are all over the place these days speaking in support of things like their quarterly Summary of Economic Projections (SEP).

President Trump takes it to another level when he says Warsh is “from central casting.” The nominee himself seems to favor a lower profile, if perhaps only from a policy perspective. Indeed, as Deutsche Bank Chief U.S. Economist Matthew Luzzetti writes, “Consistent with his prior comments, Warsh was highly critical of Fed communications, especially forward guidance.”

And it’s mostly about the dot plot.

“The Fed tells the whole world what their dots are going to be, what their forecasts are going to be,” Warsh said of the SEP during his testimony before the Senate Banking Committee. “Well, the Fed’s human. And then they hold on to those forecasts longer than they should.” Warsh alludes to “confirmation bias”: our tendency to focus on information that supports our current view and exclude information that contradicts it.

(Image credit: Getty Images)

“If the Fed were to wait until it gets into a meeting before making a decision,” Warsh believes, “incremental deliberation can keep the central bank from compounding its errors.” The dot plots, as Warsh sees them, promise transparency but, ultimately, undermine credibility. “I think these are big changes that are needed,” the nominee told the committee, “and if confirmed, I look forward to doing it.”

As Luzzetti notes, Warsh called for “regime change” in Fed communications. “That said,” the economist adds, “he did not propose specific changes to these communication tools or practices.” Nor did Warsh say whether he will or will not continue with post-FOMC-meeting press conferences.

“If you ask me my true personal opinion right now,” Warsh said, “Fed chairs and other central bankers around the FOMC, they speak quite frequently. I would say this: I think truth-seeking is more important than repetition. If one has a press conference, one wants to deliver some important news.”

A new inflation gauge

As Warsh sees it, neither PCE nor CPI is a sufficient barometer of price stability. He said during his confirmation hearing that his preferred instruments are “trimmed averages” that “take out all of the tail risks, all of the one-off items” to measure the “generalized change in prices.”

A “trimmed-mean” average excludes a set percentage of the largest and smallest values in a dataset prior to calculation. Deutsche Bank economist Justin Weidner identifies “one clear benefit” to using them.

(Image credit: Getty Images)

“Inflation is measured imprecisely,” Weidner explains, “so excluding some of the ‘noise’ of large moves in smaller categories (which do not necessarily have to be food or energy categories) can provide a clearer picture of the trend.” At the same time, as Weidner notes, “Fundamental to this is the premise that the inflation prints out in the tails are in fact noise and thus not informative about the trend.”

Indeed, a May 2008 Dallas Fed staff paper (pdf) found that trimmed-mean averages are “more useful in low inflation environments, when the underlying signal is weak relative to the noise in the data.” But they may not be able to capture changes in the inflation regime information in the tails may help identify.

Lender of last resort

Gillian Tett of the Financial Times raises a compelling question in the aftermath of Warsh’s confirmation testimony: Who will organize a collective global response if another financial crisis hits? Tett refers to how Warsh answered a question asked by Sen. Jim Banks (R-Indiana) about the dollar and its position in the world.

“If confirmed as chairman of the Federal Reserve,” Warsh replied, “I will then have to say that it’s the Treasury secretary’s business to talk about the dollar. It’s the Fed chairman’s business to talk about interest rates.”

Elaborating on his position, Warsh conceded there are “risks to the U.S. position in the world, including economic” and from state actors. He highlighted the “economic statecraft agenda led by Secretary Bessent and Secretary Rubio,” referring to the respective heads of the Treasury Department and the State Department.

(Image credit: Getty Images)

“The Fed will play a supporting role in ensuring that the financial system is as safe as it can be and work with them,” Warsh said, “because it’s outside of the conduct of monetary policy to ensure the U.S. is on its front foot and in a position of strength during this period of rivalry between the U.S. and another nation around the world.”

The war in the Middle East and its impact on oil prices has generated fears of another financial market crisis. Indeed, as Tett notes, Treasury Secretary Scott Bessent confirmed that the United Arab Emirates and “numerous” other states in the region have asked for dollar swap lines. Bessent and the Treasury extended a $20 billion swap line to Argentina in 2025.

Dollar swap lines were the critical tools then-New York Fed President Timothy Geithner used to calm financial markets during the global financial crisis in 2008-09, using existing arrangements with five central banks and temporary arrangements with nine others.

Warsh has signaled his agreement with the “geoeconomics” practiced by Trump, Bessent and Secretary of State Marco Rubio. A global risk here, as Tett writes, “is that dollar swap lines will become increasingly weaponised. For while the Fed has always tried to downplay the role of geopolitics in its own swap lines, Bessent says he wants to use swaps to promote American dominance and reward allies, ‘locking in dollar supremacy’.”