Target (TGT) is one of the oldest and most iconic brands in American retail, but shares in the national discount chain have been a bad buy-and-hold bet for ages.

The big-box chain that came to define the concept of “cheap chic” traces its roots to a single family-owned department store in the early days of the 20th century. Six decades later, a rapidly expanding middle class in the midst of the baby boom drove consumer demand for one-stop shopping at value prices. It’s no coincidence that Target shifted to a discount format at the same time that Walmart (WMT) and K-Mart entered the market.

A merger and decades of expansion set Target up to be the comparatively upscale alternative to Walmart during the heyday of big-box chains at the end of the 20th century. Whereas Walmart’s slogan was “Always Low Prices, Always,” Target led with “Expect More. Pay Less.”

Sign up for Kiplinger’s Free Newsletters

Profit and prosper with the best of expert advice on investing, taxes, retirement, personal finance and more – straight to your e-mail.

Profit and prosper with the best of expert advice – straight to your e-mail.

By the beginning of the 21st century, the Minneapolis-based chain was a certified national retail behemoth. And then things started to go wrong.

The onslaught of Amazon.com (AMZN) and other e-commerce companies took a toll on all brick-and-mortar retailers. Chronic underinvestment in its digital strategy caused Target to fall far behind Walmart in the rapidly growing channel. Today, Walmart is the second-largest U.S. e-commerce retailer after Amazon – albeit a distant second. Target, meanwhile, ranks fifth.

A massive data breach in 2013 that exposed the financial information of as many as 110 million Target customers certainly did the company no favors. Even worse was Target’s abortive expansion into Canada. The foray, which lasted only two years, ended in 2015 with the company shuttering 133 stores and taking a $5.4 billion quarterly loss.

Target’s product mix also makes it more sensitive to economic ups and downs. Where Walmart’s and Costco’s (COST) top lines benefit from consumer staples that tend to hold up better when consumer spending slows down, Target depends more on discretionary items. Food, toilet paper and diapers are more recession-proof than apparel and consumer electronics.

More recently, Target’s margins have been hampered by shrink – the loss of inventory due to theft, damage or administrative error – and tariffs. A decade ago, the company enjoyed gross profit margins north of 27%, or more than two percentage points higher than they run today.

It should come as no surprise that a turbulent couple of decades haven’t been great for TGT stock.

The bottom line on TGT stock?

True, Target is a dividend-raising machine. Equity income investors have seen their payouts rise annually for more than five decades. As a member of the S&P 500 Dividend Aristocrats, there’s no doubt that TGT is one of the best dividend stocks for dependable dividend growth.

Sadly, a poor track record of price appreciation wipes out the benefit those dividends contributed to shareholders’ total returns.

For its entire life as a publicly traded company, Target generated an annualized total return (price change plus dividends) of just 5.4%. That lags the S&P 500 by more than 5 percentage points.

And while the consumer staples stock is up 38% over the past 52 weeks – vs 31% for the broader market – every other standard time frame is a dud. Shares in TGT generated negative total returns over the past three- and five-year periods. As for the past 10- and 15-year periods, TGT lags the S&P 500 by wide margins.

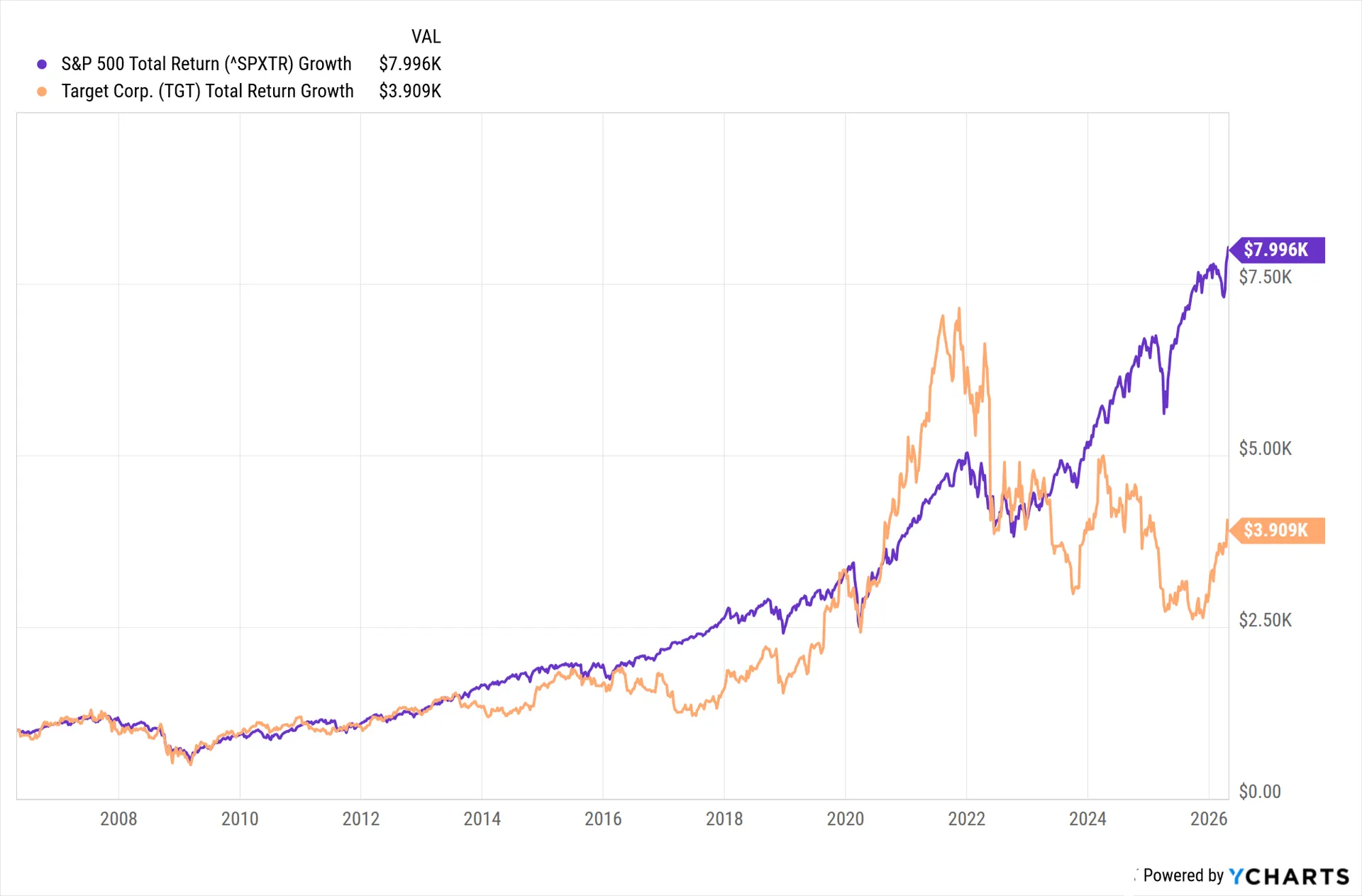

Which brings us to what you’d have if you invested a grand in TGT stock a couple of decades ago.

Spoiler alert: not nearly enough.

Take a look at the chart above and you’ll see that if you put $1,000 into TGT stock 20 years ago, it would be worth about $3,900 today. That’s good for an annualized total return of 7%.

The same sum sitting in a low-cost S&P 500 index fund over the past two decades would be worth almost $8,000 today, or 10.8% annualized.

There’s no way around it: Target has been a buy-and-hold bust for truly long-term investors.

As for where TGT stock goes over the next 12 months or so, Wall Street is very much split on the name. Of the 37 analysts covering the stock surveyed by S&P Global Market Intelligence, 9 call it a Strong Buy, two say Buy, 23 have it at Hold and three rate it at Sell. That works out to a consensus recommendation of Hold.