Mandy Xu

▬

February 23, 2026

Link to Report: Macro Volatility Digest

WHAT STANDS OUT:

- Implied volatilities diverged last week on the back of rising geopolitical tensions, changing tariff policy, and lingering AI worries. Commodity vols saw the biggest increase, with oil 1M implied volatility jumping over 12 pts to 52% on fear of an US-Iran conflict. Oil skew is the most inverted (calls trading at a premium to puts) since the 2022 Russia-Ukraine invasion, with the inversion extending out to the 6M tenor as traders position for a period of prolonged geopolitical tension. In contrast, equity and rates vol all ended the week lower after the Supreme Court struck down Trump’s emergency tariffs though uncertainty remains around new/additional tariffs.

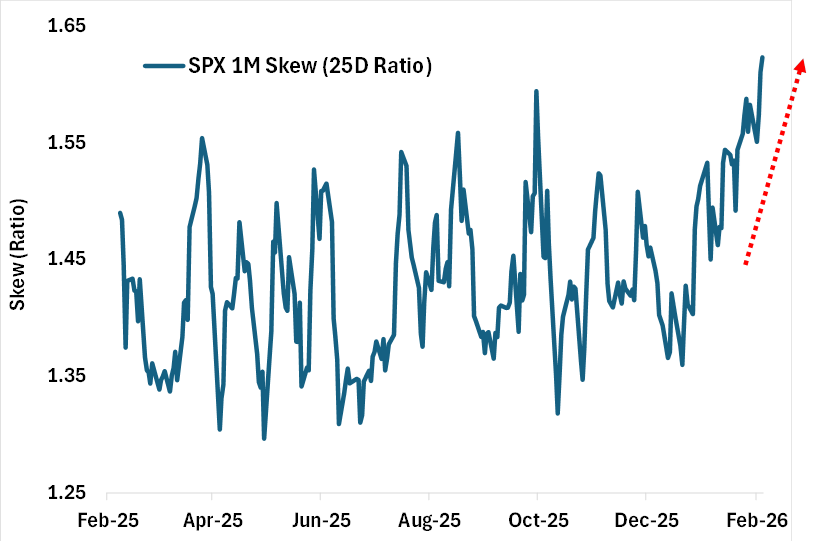

- SPX 1M skew steepened to a 1-year high last week (see chart below). Notably, skew is rich not just for the front-month tenor but across the term structure, as longer-term risks rise. Despite earnings season wrapping up, single stock vol also remains remarkably bid as stocks continue to see outsized moves on the back of AI, tariff, and policy risks. Expected dispersion, as measured by the DSPXSM index, is just 2 pts below its recent pre-earnings season high of 38%.

- Small cap stocks have outperformed YTD, up 7% vs. SPX index. Interestingly, skew has also steepened despite the outperformance, with RTY 1M skew jumping to the 94th percentile high on the back of strong hedging demand. Can small caps continue to outperform? Join us this Wednesday 12:30pm ET as we discuss the outlook for small caps with FTSE Russell (register here for the webinar).

Chart: SPX Skew Steepens to 1Y High

Source: Cboe