Longtime shareholders in Micron Technology (MU) used to be longtime sufferers. Not anymore.

The company for decades plodded along in the volatile, low-margin business of making computer memory chips. That’s a tough racket. Chips are a commodity. They’re cyclical. Meanwhile, chipmakers have to constantly plow cash into research and development — to say nothing of capital expenditures — just to keep pace with peers.

Micron escaped its formerly poky past thanks to the era of artificial intelligence (AI). The ongoing build-out of AI infrastructure isn’t just creating massive demand for specialized chips from the likes of Nvidia (NVDA); it’s also fueling a run on companies that supply storage. Demand for Micron’s wares — Dynamic Random-Access Memory (DRAM), NAND Flash memory, Solid-State Drives (SSDs) and Ultra High Bandwidth Memory (HBM) – has absolutely exploded.

Sign up for Kiplinger’s Free Newsletters

Profit and prosper with the best of expert advice on investing, taxes, retirement, personal finance and more – straight to your e-mail.

Profit and prosper with the best of expert advice – straight to your e-mail.

The once-ugly duckling is now a swan. And with shares up more than 850% over the past year, MU stock is no longer a long-term laggard. Indeed, it’s been an improbably good bet for truly patient investors.

The lone major American computer memory manufacturer is one of the industry’s “Big Three.” It competes on the global stage with South Korean heavyweights Samsung (SSNLF) and SK Hynix (HXSCL). And business has never been better.

That’s not too shabby for a company that was founded in the late 1970s in the basement of a dental office in Boise. Along the way, Micron helped lead the way in the development of memory chips, demonstrating a particular strength in increasing density. With more than 60,000 patents, it’s an engineering powerhouse.

But the grim realities of relentless R&D and capital expenditures in an industry where chip prices regularly plummet made Micron a tough stock to love. Anyone who couldn’t stomach prolonged drawdowns of anywhere from 40% to 70% did not belong in the name.

The bottom line on MU stock?

Micron’s red-hot run has done wonders for its returns over every standardized investing period you care to look at. For its entire life as a publicly traded company, MU generated an annualized total return (price change plus dividends) of almost 21%. That beats the S&P 500 by about 11 percentage points.

More recent results are simply stupendous. Over the past three years, MU returned 133% vs 23% for the broader market. The five-, 10- and 15-year return periods delivered massive outperformance as well.

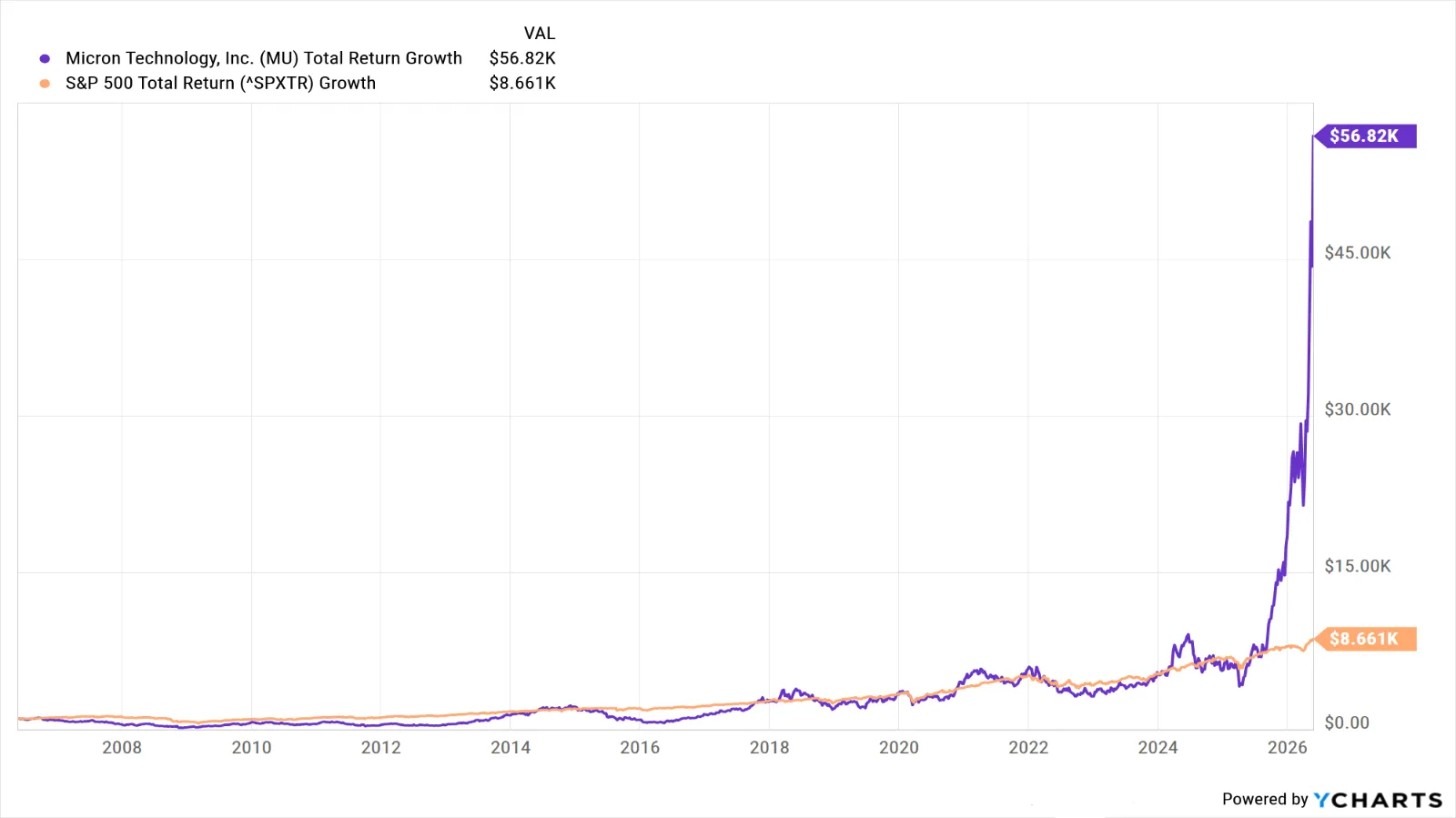

Which brings us to what $1,000 invested in Micron stock 20 years ago would be worth today.

Have a look at the above chart and you’ll see that a thousand bucks invested in MU two decades ago would today amount to almost $57,000. That’s good for an annualized return of nearly 23%.

By comparison, the same sum socked away in an S&P 500 index fund would be worth about $8,600 today – or 11.4% annualized.

Will the good times keep rolling for this darling of an AI play? Wall Street sure thinks so.

“This is the memory bottleneck trade where the company can’t nearly supply the backlog of orders,” writes David Miller, chief investment officer at Catalyst Funds. “AI workloads need a huge amount of high bandwidth memory and storage. Micron gives you a way to play that part of the AI buildout at a reasonable forward earnings multiple.”

Miller’s views are widely shared. Of the 44 analysts covering MU stock surveyed by S&P Global Market Intelligence, 39 rate it at Strong Buy, nine say Buy and four call it a Hold. One analyst rates it at Strong Sell. Nevertheless, that works out to a consensus recommendation of Strong Buy, with high conviction to boot.