Mastercard (MA) shareholders might not be too thrilled with the stock’s more recent run, but few names have treated buy-and-hold investors to better returns over the long haul.

The world’s second-largest payments processor has lost some of its luster over the past few years, but that’s more to do with the legal and regulatory landscape than the company’s operations. Threats to Mastercard’s duopoly with Visa (V) are overblown, bulls say, and shares are priced for future outperformance for patient investors.

Buy-and-hold types who’ve been in the blue chip stock for ages can attest to Mastercard’s strength. And while its competitive moat might not be quite as wide as it once was, the company’s global brand remains as powerful as ever.

Sign up for Kiplinger’s Free Newsletters

Profit and prosper with the best of expert advice on investing, taxes, retirement, personal finance and more – straight to your e-mail.

Profit and prosper with the best of expert advice – straight to your e-mail.

That’s no small feat. A firm that was launched more than 50 years ago by a consortium of regional banks to compete with Visa today operates in more than 210 countries and territories. Nearly 40 million businesses accept Mastercard credit cards, of which there are 3 billion in circulation.

Payments processors aren’t all that sexy, but Mastercard has indeed notched some nifty wins for capitalism. In the 1980s, the company issued the first international payment card in the People’s Republic of China, as well as in what was then the Soviet Union.

Mastercard also has a history of innovation in security features, pioneering the now-standard practice of putting laser-etched holograms on cards. Later, it spearheaded the global rollout of the chip technology that today makes cards far more secure.

But investors were best served by the company’s transition from a bank-owned cooperative to a publicly listed company in 2006. Anyone who invested in Mastercard during those early post-IPO days should have no problem paying off their purchases.

True, shares are lagging the S&P 500 by a wide margin over the past year or so. MA hasn’t kept up with the broader market over the past half-decade either. Partly, that’s a function of the way the tech sector — and all things related to artificial intelligence (AI) — have soared since ChatGPT debuted at the end of 2022.

MA is also contending with industrywide concerns. Persistent scrutiny of swipe fees has been a headwind for years. And now, the bipartisan Credit Card Competition Act of 2026 threatens Mastercard and Visa’s lucrative duopoly. Calls to cap interest charges, while unworkable, are also spooking investors. (Shares in Visa have likewise underperformed the market for years now.)

You can see these anxieties playing out in Mastercard’s valuation. Shares currently trade at less than 22 times estimated earnings. That’s 20% lower than their five- and 10-year averages. A stock that once commanded hefty premiums thanks to its high operating margins (nearly 60%) and wide competitive moat has been repriced to reflect rising risks.

Interestingly, Berkshire Hathaway (BRK.B) sold its stakes in both Mastercard and Visa during the first quarter of 2026. The payments processors had been a couple of Warren Buffett’s favorite stocks since 2011. Apparently, CEO Greg Abel, who is now calling the shots, sees things differently. Make of that what you will.

The bottom line on MA stock?

As noted above, Mastercard stock has been disappointing for more recent investors. Shares lag the broader market on an annualized total return basis (price change plus dividends) over the past one-, three- and five-year periods. Heck, over the past 52 weeks, MA stock is off about 4% vs a 30% gain for the S&P 500.

Beyond those recent periods, however, the returns have been priceless.

Over the past decade, MA stock leads the broader market by almost 3 percentage points. Over the past 15-year period, it beats the S&P 500 by more than 7 points.

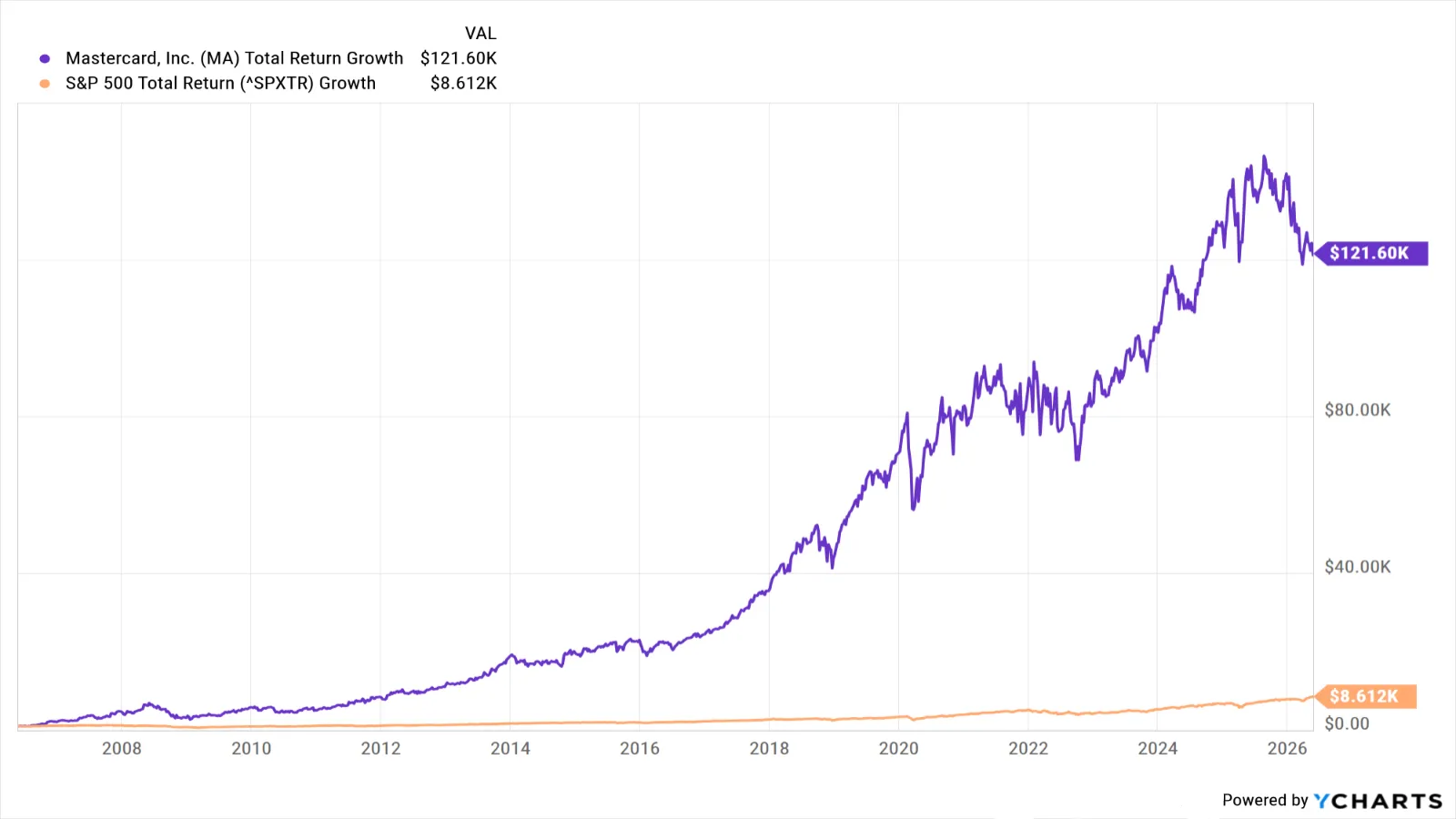

Which brings us to what $1,000 invested in Mastercard stock 20 years ago would be worth today. Spoiler alert: a lot.

(Image credit: YCharts)

Have a look at the above chart and you’ll see that a thousand bucks invested in MA stock two decades ago would today amount to almost $121,000. That’s good for an annualized return of more than 27%.

By comparison, the same sum socked away in an S&P 500 index fund would be worth about $8,600 today – or 11.4% annualized.

That’s remarkable outperformance. Happily for bulls, Wall Street analysts think Mastercard is priced to resume its winning ways.

“Solid quarterly earnings again underscored the resilience of MA’s operating model amid a more mixed payments and macro backdrop,” writes BofA Securities analyst Matthew O’Neill, who rates shares at Buy. “The underlying constant currency demand outlook remains intact, supporting confidence in Mastercard’s long-term earnings durability and capital return profile.”

O’Neill has plenty of company on the Street. Of the 39 analysts covering MA stock surveyed by S&P Global Market Intelligence, 29 rate it at Strong Buy, seven say Buy and three call it a Hold. That works out to a consensus recommendation of Strong Buy, with high conviction to boot.