Balance Is Not Exactly an ‘Easy Rider’ Trip")

Dennis Hopper and Peter Fonda in the 1969 film, “Easy Rider.”

(Image credit: Silver Screen Collection/Hulton Archive/Getty Images)

The baby boomer generation exploded onto the American cultural and economic landscape in 1946, becoming the wealthiest generation in American history. Like the rule-breaking characters of “Easy Rider,” boomers claimed the right to more freedom to shape their lives than their parents had enjoyed. In the same vein, they have had to reinvent what it means to have leisure time, to work and retire. But though boomers (born in 1946 to 1964) haven’t gloriously burned out, as Neil Young’s anthem extolled, they also haven’t “faded away.”

Their fate has got to be better than that of Easy Riders’ Billy, Wayne and George.

The older boomers of the Woodstock era now worry about the long-term viability of their retirement, while younger boomers (who identify more with Star Wars than Woodstock) are sweating over their retirement readiness.

Sign up for Kiplinger’s Free Newsletters

Profit and prosper with the best of expert advice on investing, taxes, retirement, personal finance and more – straight to your e-mail.

Profit and prosper with the best of expert advice – straight to your e-mail.

Of course, retirement wasn’t a top priority for the boomers at Woodstock (heck, the 401(k) wasn’t invented until nine years after the last chords faded away from Hendrix’s “Hey Joe” at the legendary music festival). But the size of their nest egg, nearly 60 years later, is a prime concern.

With the average boomer 401(k) account balance clocking in at $270,800 at the end of 2025, according to Fidelity’s Q4 2025 Retirement analysis — falling well short of the $1.46 million ‘magic number’ that American workers think they’ll need to retire comfortably, according to Northwestern Mutual — there’s reason for concern. In fact, four of 10 Boomers think it’s likely that they will outlive their savings, according to Northwestern Mutual’s 2026 Planning & Progress Study.

| Header Cell – Column 0 |

Boomers |

All 401(k) savers |

|---|---|---|

|

Average balance |

$270,800 |

$146,400 |

|

Employee savings rate |

12.10% |

9.50% |

|

Employer contribution rate |

5.00% |

4.70% |

|

Percentage of workers who increased contribution rate |

9.60% |

11.20% |

|

Percentage contributing to a Roth 401(k) |

13.90% |

18.00% |

|

Percentage with all their 401(k) savings in a target-date fund |

45.40% |

63.00% |

|

Percentage with outstanding 401(k) loan |

14.00% |

19.40% |

|

Percentage who made a change to their asset allocation |

6.80% |

5.40% |

But there’s good news about boomer 401(k) balances, too

A review of Fidelity data highlighting 401(k) balances for boomers who have contributed to the same workplace retirement plan for 5, 10, or 15 consecutive years casts a more positive light on their retirement readiness. Boomers, for example, who have socked away money in their 401(k)s starting in 2010, have an average balance of roughly $600,000, just shy of the $617,600 average for all 401(k) savers, according to Fidelity. Boomers in their 60s have an average balance of $269,100, and retirees 70 and older have an average balance of $273,100, according to Fidelity data.

“The long-term savings data is perhaps more accurate,” says Jonathan Lee, a wealth management advisor at U.S. Bancorp Advisors. In his work with clients, he says it’s not uncommon for workers who have been at one job for a long time to also have other retirement savings balances from prior jobs that they’ve kept at their old employer or rolled into an individual retirement account (IRA).

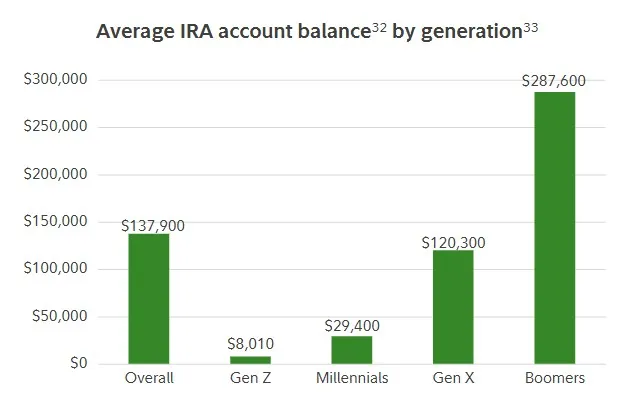

His point is backed up by data. A review of Fidelity’s fourth-quarter 2025 data shows that boomers, on average, have $287,600 in IRA savings, too. And Boomers 70 and older have $332,784 saved in their IRA. That extra savings brightens the picture for boomers, especially for those who also have 401(k)s. Looking at all the different sources of retirement savings, Lee says, paints a more realistic picture of total savings.

33. Fidelity business analysis of 18.9 million IRA accounts as of December 31, 2025. Considers only active participants with a balance. 33. Generations as defined by Pew Research.

Lee also stresses that looking at average balances through the lens of an entire generation may offer less insight than you think regarding your own retirement readiness. “Don’t be so fast to compare yourself to your whole generation,” says Lee. “Your situation, your goals, and your lifestyle are different.”

Boomer savings trends, on average, tend to be pretty solid. The average boomer who is still working saves 17.1% of their salary (including their employer’s matching contribution), which tops Fidelity’s recommended 15% savings rate. And nearly one in 10 boomers increased their contribution rate last year.

Boomers’ savings versus the recommended amount by age

When it comes to Fidelity’s savings guidelines that measure savings targets by one’s age and salary, boomers are doing just OK. Fidelity recommends that savers have 8 times their salary saved by age 60. But just 37% of boomers have that much saved (even though they are older than 60), according to Northwestern Mutual’s 2026 study. And only 29% of boomers have more than 10 times their salary saved, which Fidelity says is a benchmark for savers by age 67.

But the fact that the average Boomer 401(k) balance is roughly $271,000, far from the seven-figure balance most people think they’ll need, suggests that many members of the nation’s oldest generation have a savings gap that must be filled.

The good news is that the youngest Boomers are just 62 years old, giving them at least five more years to work and save before they reach age 67, a common retirement date as it coincides with full retirement age (for workers born in 1961 or later) in the eyes of the Social Security Administration.

|

Total saved as a multiple of income |

Boomers |

All retirement savers |

|---|---|---|

|

Less than 1x my income |

7% |

15% |

|

1x |

5% |

8% |

|

2x |

6% |

13% |

|

3x |

10% |

15% |

|

4x |

7% |

7% |

|

5x |

7% |

8% |

|

6x |

4% |

4% |

|

7x |

5% |

4% |

|

8x (ideal savings by age 60) |

5% |

4% |

|

9x |

3% |

2% |

|

10x (ideal savings by age 67) |

8% |

4% |

|

More than 10x my income |

21% |

10% |

|

Not sure |

7% |

7% |

How boomers with 401(k) shortfalls can play catch-up

Creating a nest egg that’s built to last is not just about poring every available dollar into a tax-deferred retirement account. Blake Smith, an investment advisor at Financial Partners, Inc., says every worker and retirement saver should ask themselves: “Where are those retirement dollars located?” Is all your money in a traditional pre-tax 401(k) or a Roth account that’s taxed upfront but offers tax-free withdrawals?

The answer is key, as it will impact how long your money will last once you start taking distributions, Smith says. “Not all money is taxed the same,” says Smith. “A million dollars sitting in a traditional 401(k) (that is taxed as ordinary income) is very different from $1 million in a tax-free Roth.”

Just like a paycheck in the working world, a retirement account balance must be viewed in the context of what you can bring home after taxes. “A huge part of the planning conversation is not only what a client’s account balance is, but what is the future tax nature of those account balances,” says Smith.

Consider this example. Let’s say you need to net $50,000 from a retirement account to pay for your daughter’s wedding. If you have the cash sitting in a tax-free Roth account, you only need to withdraw $50,000. However, if all your money is in a traditional 401(k), which treats withdrawal amounts as regular income, and you are in the 22% tax bracket, you will have to withdraw $64,103 to meet your $14,103 tax obligation to the IRS.

That’s why Smith says so-called “tax diversification” of your retirement savings is just as important to portfolio diversification.

(Image credit: Getty Images)

Retirement challenge for Boomers: unwinding years of tax-deferred savings

As a result, the game plan for many boomers nearing retirement is to “unwind many years of tax-deferred savings” to avoid a so-called tax torpedo later when required minimum distributions (RMDs) start at age 73 and result in large tax bills because the withdrawals are taxed at ordinary income rates, which can go as high as 37%, says Smith.

(Image credit: Getty Images)

Why Roth conversions make financial sense

Smith recommends that boomers take advantage of the low tax rates that were made permanent by the passage of the One Big Beautiful Bill in July 2025. “We don’t want to let this current window of low tax rates close,” says Smith. “We get to keep these historically low tax years for years to come.”

Doing Roth conversions when taxes are low allows you to pay less to the IRS on the amount of assets you convert. For younger boomers with years to go before retirement and Social Security kicks in, a good strategy is to move money from traditional pre-tax 401(k)s and IRAs into Roths over a number of years to minimize your annual tax hit and to lower your balances before RMDs kick in at age 73.

Another way to unwind higher-tax savings sitting in traditional retirement accounts is to withdraw more money than you need from these accounts to tactically lower your balance in the years before RMDs start, says Smith.

Take advantage of catch-up contributions

If you’re facing a retirement savings shortfall, play catch-up. The IRS offers a number of opportunities for retirement savers ages 50 and older, as well as those between 60 and 63, to save more in their accounts. “Take advantage of these higher catch-up contribution limits,” says Smith.

The regular contribution limit for 401(k)s in 2026 is $24,500. But workers 50 or older can sock away an additional $8,000 in catch-up contributions. And workers ages 60 through 63 can save an additional $3,250 in a “super” catch-up. That’s a maximum savings of $35,750 in 2026.

A new Roth catch-up mandate created in the One Big Beautiful Bill forces high-income earners aged 50 and up with prior-year FICA wages over $150,000 to designate all catch-up contributions to a Roth 401(k) using after-tax dollars. While the new rule does away with an up-front tax deduction, it’s a way for savers to begin to diversify their retirement dollars from a tax perspective by funneling more funds into tax-free Roths. “It’s an opportunity to accelerate savings into the future and take advantage of these low brackets,” says Smith, adding that it also gives savers who have no Roth accounts a way to open an account and start the five-year timeframe before they’re able to access the Roth money penalty-free. “The quicker that clock starts counting, the quicker you can satisfy the five-year rule.”