Link to Report: Macro Volatility Digest

WHAT STANDS OUT:

- Implied volatilities normalized across asset classes last week as momentum built toward a peace deal between US and Iran. Equity, rates, credit, and FX implied volatilities all fell below their long-term averages. WTI 1M implied vol collapsed by nearly 30 pts wk/wk to 47% – though notably we still see strong demand for call options with oil skew remaining inverted. This suggests that despite widespread optimism of an imminent deal, oil traders still see elevated risk of a prolonged conflict – a prescient call given the weekend developments.

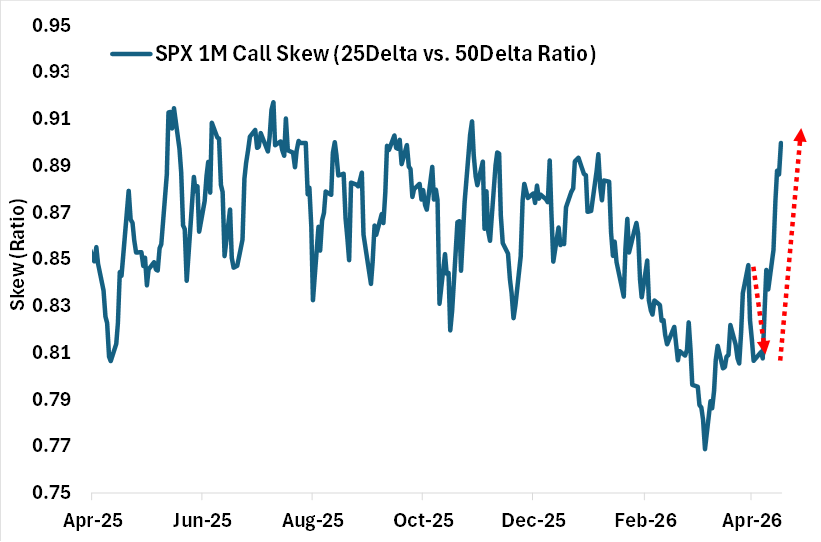

- When equities first bottomed out at the end of March, options traders were initially skeptical of the rally with most of the initial activity focused on fading the rebound. But since April 8th, that has changed dramatically. SPX 1M call skew, a measure of demand for upside calls, has surged from near a 1-year low to now the 90th percentile high on the back of FOMO (see chart below). Put skew, conversely, has fallen to the 15th percentile low with hedgers largely throwing in the towel.

- As macro risks fade, investor focus is shifting back to the AI trade ahead of upcoming earnings. This can be seen in the elevated levels of single stock volatility, as well as the outperformance of mega-cap Tech with the Cboe Magnificent 10 Index (ticker: MGTN) up over 22% since March. We’ve seen a notable pickup in retail activity in MGTN options recently, with retail flow now making up over 80% of the volume and 0DTE options jumping to 32% of the overall volume in April.

Chart: Upside Chasing Evident in SPX Options

Source: Cboe