The newest fund, IBIM, holds just one TIPS, but will expand. I have cautions.

By David Enna, Tipswatch.com

Blackrock’s iShares division in March launched a unique ETF holding just one bond: CUSIP 91282CPU9, a 10-year TIPS that matures in January 2036.

The formal name is the “iShares iBonds Oct 2036 Term TIPS ETF,” with the ticker IBIM. The goal: To track the performance of U.S. Treasury Inflation-Protected Securities maturing in 2036. Later this year IBIM will add a second TIPS, to be issued in July, and then add two more 5-year TIPS to be issued in April and October 2031.

This is the 11th currently existing ETF of this type, holding TIPS maturing in a certain year. Others, such as IBIA and IBIB, have now matured. I have been following these funds for several years, and as time passes, I am easing off my initial qualms: Too weird and too small to be successful.

I had questions: Who is the target market for an ETF that will be holding only two to six bonds until maturity? Why not just buy and hold the individual TIPS? Would these ETFs provide tax-reporting benefits in a taxable account? Are these ETFs targeted at customers of assets-under-management financial advisers (which would possibly increase the cost to investors)?

The iShares suite of defined-maturity TIPS funds currently offers maturities for 2026 to 2036. Ideally, you buy the ETF — intending to hold to maturity — and then after a defined period, it distributes all proceeds and closes down. You can download the prospectus for the new 2036 fund here and the fact sheet here.

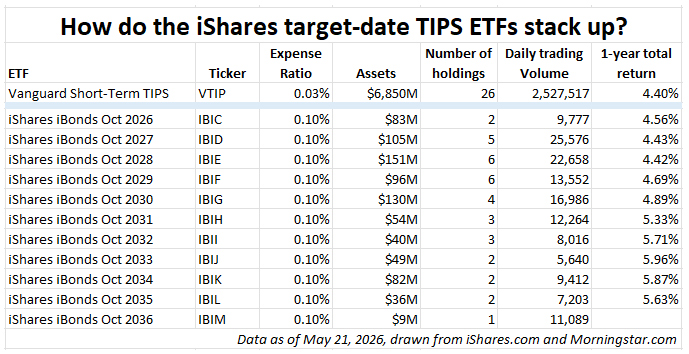

iShares has said these ETFs are designed to “mature like a bond, trade like a stock.” These are useful ETFs, I think, especially for an investor looking to quickly build a diversified TIPS ladder out to 2036. These funds should closely track the performance of the underlying TIPS. Here is a comparison of data for each ETF, along with VTIP, Vanguard’s Short-Term TIPS fund, for comparison:

The expense ratios for the iShares ETFs are only 0.10%, higher than VTIP’s 0.03% but quite good for such small funds.

Analysis

These funds are designed to be held to maturity and the asset value will rise and fall with market trends through maturity, just like any other bond fund.

Because the expense ratio is just 0.10%, I really have no problem with using these funds as an alternative to buying individual TIPS. You could quickly build a ladder through 2036 in 15 to 30 minutes.

However, the limited span of maturities means these ETFs aren’t the total solution for building an inflation-protected ladder of investments to cover 20 to 30 years. I raised this point in an April interview with Jason Zweig of the Wall Street Journal. He wrote:

You could use them as a “bridge” to Social Security if you’ll be retiring within 10 years, says David Enna, editor of Tipswatch.com. They aren’t yet a complete solution if you want to protect your purchasing power for, say, the next 30 years.

The size and trading volumes of these funds have increased nicely over the last two years, but still remain small compared to VTIP, an ETF giant. I suspect the ETFs are attracting many investors working with financial advisers. TIPS are complicated, and these funds are much easier to grasp.

The ETF trades as stock, so there is no minimum investment required. The cost of one share of IBIM was $25.13 at the close on Thursday. However, investors could face some bid-ask issues for very large orders.

Income and inflation accrual distributions

One of the advantages of owning a TIPS to maturity is that inflation accruals continue to build over time, increasing the amount of principal and also increasing the semi-annual coupon payment as the principal increases. An individual TIPS gets the benefit of compounding, even though the coupon is distributed twice a year.

But one of the disadvantages of a TIPS is that if held in a taxable account, those inflation accruals are subject to “phantom” federal income taxes in the current year, even though they are not paid out. Plus, if your account is at TreasuryDirect, you will face the “dreaded 1099-OID,” the cryptic form reporting your taxable accruals.

The ETF plus. These defined-maturity ETFs “fix” the OID issue because inflation accruals will be paid out in the current year, along with the coupon interest. (This is the same way traditional TIPS funds work). That distribution makes these iShares TIPS ETFs more attractive for holding in a taxable account, because it eliminates the phantom income problem.

I assume this also means your broker will provide a single 1099-DIV tax form covering both coupon payments and inflation accruals.

The ETF minus. Distributing the inflation accruals in the current year means that at maturity you will be receiving only the original par value and final coupon payment, since all the inflation accruals would have been distributed. Zweig noted this in his April article:

Like all TIPS mutual funds or ETFs, the iShares funds pay out the inflation adjustment as current income each year. With individual TIPS, the inflation adjustment builds over time as an increase in principal value that isn’t realized until maturity or sale. In either case, the adjustment is taxable outside a retirement account.

In essence, this means if you buy IBIM at around $25 a share this week, in 2036 you are going to get back about $25 at maturity, but you will have earned inflation accruals and coupon payments along the way.

To get the full benefits of compounding and true inflation protection you would need to reinvest all inflation-accrual distributions back into these TIPS ETFs or another similar product. That could be a problem because of the low trading volume. I don’t own these ETFs, but it appears that Fidelity and Schwab do allow reinvestments, and Vanguard … might.

I have gotten feedback from readers saying they have been able to reinvest the dividends in these low-volume funds. Beyond the cost of any bid-ask spread, that is great news. If anyone has further experience with buying these funds and/or reinvesting the dividends, please provide the information in the comments section.

Do you need cash flow? To recap, these ETFs offer a cash-flow solution if held in a taxable account, with coupon interest and inflation accruals being paid out (and taxable) each year. If you don’t need the cash flow and are going to reinvest the dividends, they would work better in a tax-deferred account.

Thoughts

I buy individual TIPS with the intention of holding to maturity, so I already own CUSIP 91282CPU9 maturing in January 2036. But I can see the appeal for investors looking for a simpler way to invest in TIPS, especially in a taxable account.

The expense ratio of 0.10% is very good, especially if you can make your trades commission-free. But I do warn against using these ETFs in an assets-under-management account, which could wipe out 1% or more of your annual earnings. And in fact, I suspect these ETFs may have been designed for AUM financial advisers who really don’t understand TIPS (a lot of them don’t).

In summary, these target-maturity ETFs are a good investment for cash flow, would work well in a taxable account, and I really have no problem with them.

A new PIMCO ETF

On April 6, the investment firm PIMCO launched a new-fangled inflation-tracking ETF dubbed PIMCO Inflation PLUS Active ETF (PCPI). The press release says:

PCPI aims to provide investors who are concerned about rising inflation with a more direct hedge, lower volatility and limited interest rate risk versus traditional Treasury Inflation Protected Securities, known as TIPS.

PCPI is designed to limit interest rate risk and add incremental return potential through active management. It seeks real returns by investing primarily in short-term TIPS and other inflation-linked securities, and by actively managing the portfolio as market and inflation conditions change.

Sigh. This new fund might be fine, but I grit my teeth at the term “active management.” We are talking about, at most, seven TIPS and Treasury holdings? The expense ratio is 0.25%, which is eight times higher than VTIP’s 0.03%. The duration is defined as “ultra low” at 0.5 years, versus 2.5 for VTIP.

This ETF has very little trading history and I really don’t understand the premise. When a company uses the term PLUS in the ETF name in capital letters, there is something going on. Here is the prospectus if you want to dive in.

The ETF’s assets currently total $55 million, versus $6.8 billion for VTIP. This ETF is too new to draw any conclusions, but I would definitely shy away from any fund this new, this small, and this unproven.

The IVOL lesson

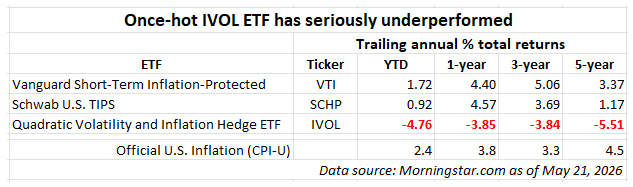

Back in the fall of 2020, when I was still writing for SeekingAlpha, I was getting a lot of questions about a new ETF with a tongue-twisting title: the Quadratic Interest Rate Volatility and Inflation Hedge ETF. Its ticker: IVOL.

The ETF’s creator, Nancy Davis of Quadratic Capital, was hailed as an innovator for this fund. Barron’s named her one of its top 200 Women in Finance in March 2020. But for me, IVOL was never particularly attractive. It was very new, with just a year of trading history. It was a fixed-income fund with a 1% expense ratio and a complex hedging strategy I couldn’t understand.

IVOL was investing 85% of its assets in SCHP, Schwab’s U.S. TIPS ETF, my favorite full-maturity-spectrum TIPS fund. On top of that, it was overlaying hedging strategies that sought to benefit from interest rate volatility. (Sound the alarms.)

IVOL had a sensational year in 2020, with a total return of 14.6% versus SCHP’s 10.9%. Readers began telling me: “This strategy works!” But In 2021, as both short- and long-term interest rates stabilized at very low levels, IVOL under-performed its two TIPS fund competitors by a wide margin.

Here are the total return results for IVOL over the last 1-year, 3-year, and 5-year periods:

Instead of looking for “new-fangled” solutions, an investor could have done much better by investing in tried and true TIPS ETFs like VTIP and SCHP. IVOL has grossly under-performing one hugely important metric: U.S. inflation.

Conclusion

Beware of the “new thing.” I don’t think the newly launched PIMCO fund is trying to push the envelope, so it may actually do fine investing in very short-term TIPS. If it is successful, let’s hope the 0.25% expense ratio begins to decline.

On the other hand, the iShares target-date TIPS ETFs have earned a look for investors who need a simplified way to buy TIPS.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I hope to keep it that way. Some readers have suggested having a way to contribute. I welcome donations, any amount. And FYI, ads on this site pay for about one visit to Costco.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.