I Bonds remain an attractive investment for capital preservation.

By David Enna, Tipswatch.com

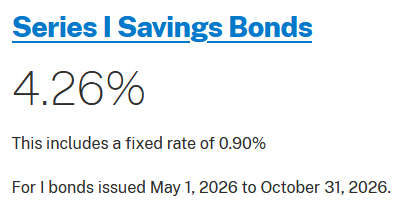

The Treasury announced this morning it is holding the fixed rate of the U.S. Series I Savings Bond at 0.90%, the rate in effect since since November 2025. This decision sets the I Bond’s six-month composite rate at 4.26% for purchases from May to October 2026.

This is exactly as I predicted, which means the Trump administration is carrying forward the basis of a decade-long formula for determining the fixed rate. That is very good news for I Bond investors.

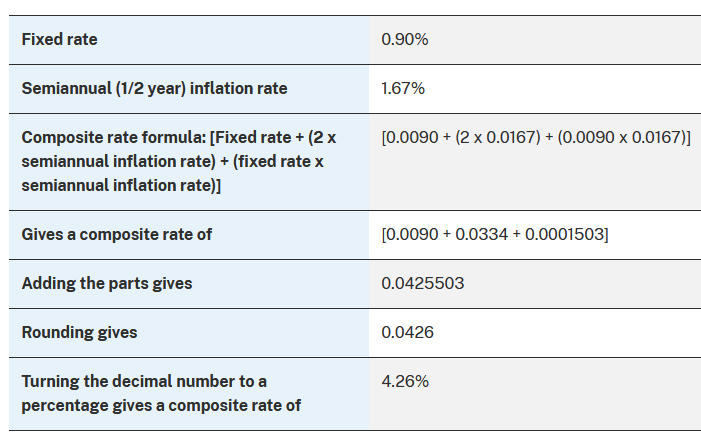

An I Bond pays interest based on a semi-annual inflation rate (in this case 1.67% from October 2025 to March 2026) and a fixed rate (which remains at 0.90%). Here is how the Treasury combines the two rates to get a composite rate of 4.26%:

The variable rate

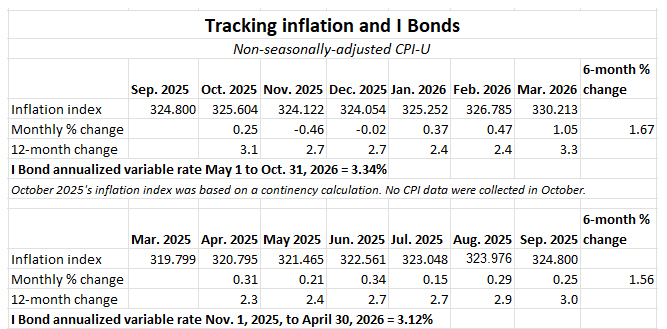

The inflation-adjusted rate (often called the I Bond’s variable rate) is now 3.34%. That rate will apply to all I Bonds ever issued, with the starting date depending on the original month of purchase. I Bonds purchased in April will get an annualized composite rate of 4.03% for six months, and then 4.26% for six months beginning in October.

The variable rate of 3.34% means that even I Bonds from past years with fixed rates of 0.0% will earn 3.34% for six months, a yield on a par with high-quality money market funds.

Here are the inflation numbers used to determine the variable rate:

The fixed rate

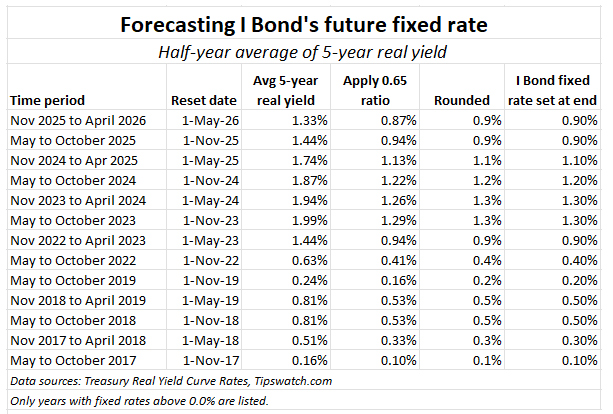

Here is the formula — devised by Boglehead geniuses — I have been using to forecast the Treasury’s fixed-rate decision: Apply a ratio of 0.65 to the average real yield of the 5-year TIPS over the last six months. This formula has worked, without fail, for 13 fixed-rate resets since November 2017. it is reassuring to see past practices continued.

The fixed rate is crucial for I Bond investors because it creates the real yield over inflation. A fixed rate of 0.90% means an I Bond will out-perform future inflation by 0.90%. This is a solid fixed rate, in my opinion, and it means your investment can continue to surpass official U.S. inflation for as long as you hold the I Bond, up to 30 years.

The composite rate

Because the fixed rate held at 0.90%, I Bonds purchased in April (too late for that now) will have a full-year return of 4.16%, combining six months of 4.03% and six of 4.26%. I Bonds purchased any time from May to October will earn six months of 4.26%, and then an undetermined composite rate based on the next rate reset on November 1.

This annualized yield of 4.26% is highly attractive in today’s market for safe investments, but keep in mind that an I Bond has to be held for 1 year and then any redemption before 5 years will lose the last three months of interest. In my opinion, I Bond investors should be looking to hold for 5 years and then cash in when they need the money.

FYI: Today’s update from the Treasury continues to carry the purchase limit of $10,000 per person per calendar year. However, it is possible to add to your holdings through gift-box, trusts, or business-owner strategies.

EE Bonds

The Treasury set the fixed rate for Series EE Bonds at 2.40% for purchases from May to October. That is down from 2.50% for purchases through April. After 20 years, EE Bonds automatically double the original purchase amount, which creates an effective return of 3.53% if held for 20 years. Treasury says:

For EE bonds you buy now, we guarantee that the bond will double in value in 20 years, even if we have to add money at 20 years to make that happen.

I suspect the Treasury gets very little investor support for EE Bonds. You can do better with short-term investments (3.75% on the 1-year T-bill) and better with long-term investments (4.97% on the 20-year Treasury note).

I Bonds remain attractive

New investors through October 2026 will be getting a six-month annualized return of 4.26%, better than the current market for short-term Treasury bills. I remain a fan of and advocate for I Bonds. I bought my 2026 allocation in April.

I Bonds work well as a secondary emergency fund, constantly adjusting to inflation. There are no state income taxes, federal taxes are deferred, the maturity date is flexible, and the value of the investment can never decline with “market trends.” You won’t get rich, but this is a strong investment for preserving capital.

If you didn’t buy in April. No problem. This was a “toss-up” decision and now you can buy in May (later in the month is wise) or better yet, just wait it out until October to decide on a purchase. On October 14, the Bureau of Labor Statistics will release the September inflation report, which will set in stone the next variable rate. And by that point we will have a pretty good idea of the next fixed rate. You’ll have a two-week period to make a decision.

If you did buy in April. If you bought your full 2026 allocation before today, you can sit back and await the November rate decision. Whatever that is, it will be available through April 2027, so the purchase cap will reset on January 1. Or … you could be daring and jump into the gift-box loophole.

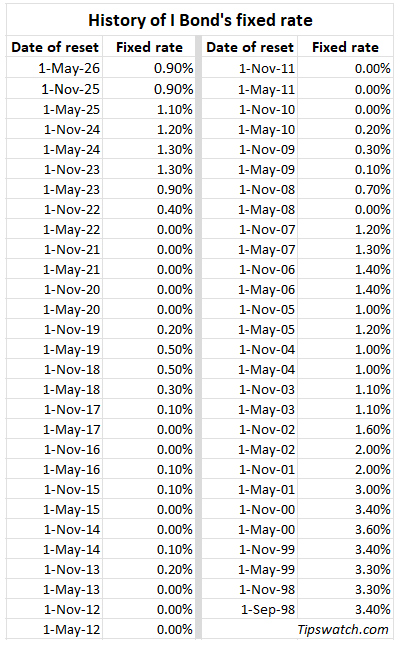

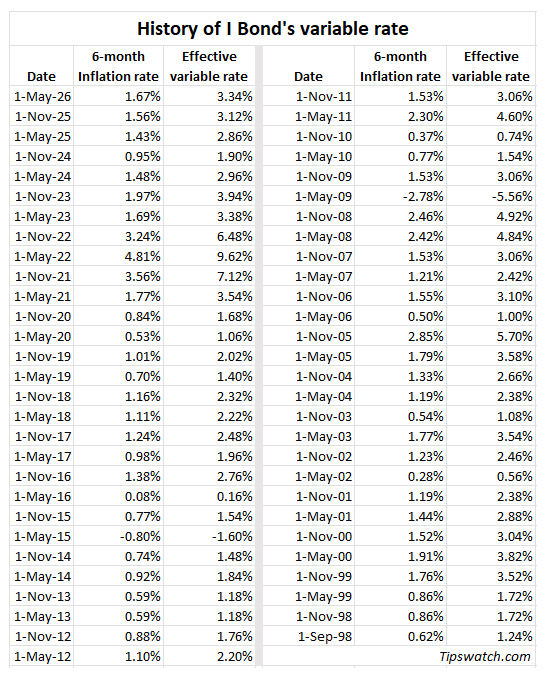

For the nerds

Here is the entire history of the I Bond’s fixed rate:

And here is the variable rate history:

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I welcome donations, any amount. And FYI, ads on this site pay for about one visit to Costco.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.