(Image credit: Getty Images)

Editor’s note: This is the fourth article in a five-part series about all-asset retirement planning that is covering such topics as using lifetime annuities and housing wealth, making the most of tax benefits and managing investment portfolio risk. The first articles are: It’s Time to Redefine Retirement for Retirees With $500,000 to $5 Million, Unlock Housing Wealth and Tax Benefits by Adding Lifetime Annuities to Your Retirement Plan and Does Your Retirement Plan Ignore Half of Your Net Worth?

So many details factor into retirement planning: Income needs, how much to leave to heirs, protection against long-term care costs and, just as important, leisure and travel.

And then there are taxes.

Sign up for Kiplinger’s Free Newsletters

Profit and prosper with the best of expert advice on investing, taxes, retirement, personal finance and more – straight to your e-mail.

Profit and prosper with the best of expert advice – straight to your e-mail.

Don’t read this article for advice on avoidance. Taxes must be paid. You can exert some control over how much you pay, however, and when you pay them.

In the first three articles of this series, we’ve talked about the components of a successful retirement plan and the Three L’s — Lifetime Income, Liquid Savings and Legacy — retirees are trying to achieve.

Of course, the success of any plan is very much determined by factors outside your control — tax laws and regulations, market volatility and your health and related expenses. We’ve tried to address the last with a new source of liquid savings in the form of HomeEquity2Income. The next article will address how to protect your plan against market shocks.

Here we’ll address the impact of taxes on the Three L’s — and how to take advantage of any tax breaks in the law, especially for income.

Detailed analysis of taxation of income

First, let’s look in more detail at how retirement plan income is taxed, including where taxes can be deferred and how rollover IRA and personal savings compare as sources of income and tax.

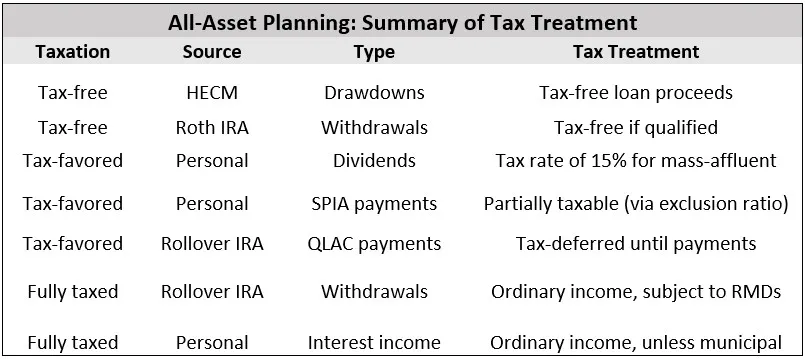

Here are the income items that make up our plans, listed by tax efficiency:

(Image credit: Courtesy of Jerry Golden)

Every retiree may not enjoy the tax advantages of each income source, but understanding what is available and how they work, separately and together, helps with planning. When we discuss legacy-related taxes later in the article, remember these income advantages, too.

Income tax objectives and measures

While there are planning models that can simulate a tax return, none, according to our research, can actually “optimize” results. The tricky part may be to prepare the correct set of more limited objectives.

Here are several measures of tax effects we’ll use in this article:

- Income tax rates at start and at age 85

- Before and after-tax return on investment (ROI)

- Percentage tax cost: Difference between before- and after-tax ROI

Because certain tax rules and our planning models use age 85 as a pivot point, in calculating the ROI, we assume consistent tax rates from the start date to age 84 and from age 85 to 95. We use the percentage tax cost in measuring the impact of taxes on all-asset planning models vs. traditional Investment-only planning.

The challenge is to create a plan that meets, as best it can, the Three L’s on a before-tax basis and to make sure that the specific allocations and elections don’t take away that advantage on an after-tax basis.

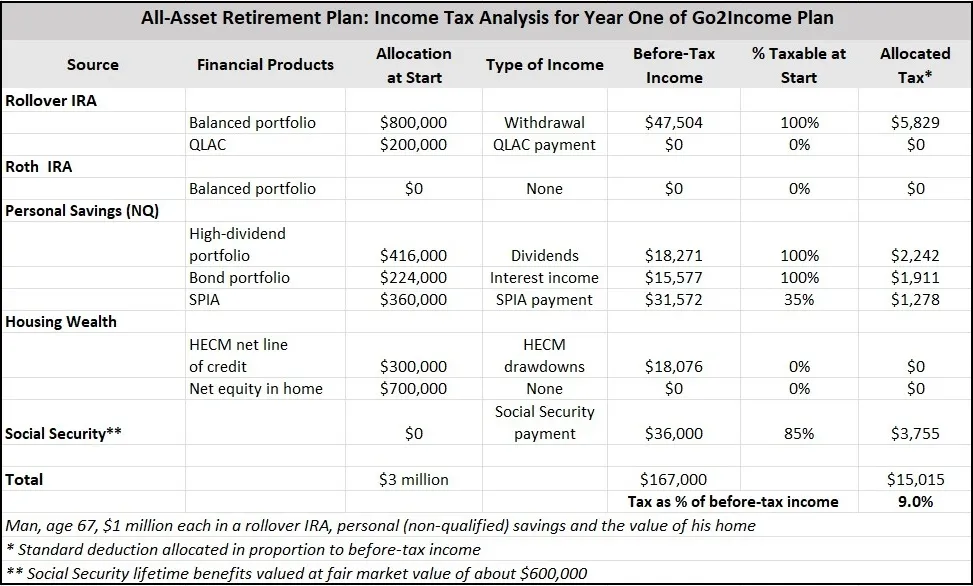

Income tax analysis for a sample investor

To show how all the pieces above fit together, we built an All-Assets Plan for a sample investor, a 67-year-old man with $1 million in each of these three buckets: Rollover IRA, personal savings and value of the house.

Set out below is a detailed analysis of the first-year tax.

(Image credit: Courtesy of Jerry Golden)

You will see there is a large amount of “safe” income in this plan, or income that is not affected by the sale of an asset, and therefore is something you can count on despite market fluctuations. In this plan, only $47,000 of IRA withdrawals out of $167,000, or 28%, require that assets be sold to generate the income.

Further, the chart is based on standard deductions, which our investor is assured of. In periods of high health-related expenses or inflation on property taxes, for instance, our investor might be able to itemize and create a larger tax deduction.

The payoff is that for this “safe” plan, the taxes represent an average of 9.0% of total income. (Note that this rate will not apply to the lifetime of a plan. The rate will vary from year to year and will increase at age 85, barring any large increase in deductible expenses.)

Compare to a traditional investment-only plan

In a traditional Investment-only plan, with no lifetime annuities and no housing wealth, the following work against tax efficiency:

- Only uses investment products without special tax benefits

- Higher allocation to fixed income portfolio with interest that is fully taxed

- No allocation to “safe” lifetime annuities and no benefit from tax incentives

- No tax-free HECM drawdowns to supplement income

- Greater need for withdrawals from IRA to generate income

Under this approach, there is a greater need for Roth conversions, which create their own tax breaks by first incurring taxable conversions.

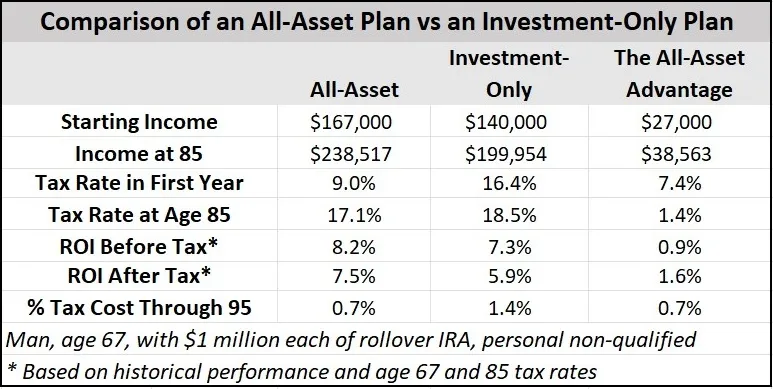

In the investment-only plan, here are the key first-year results:

- First-year income is lower at $140,000 vs $167,000

- First-year tax rate is higher at 16.4% vs 9.0%

Extending an All-Assets Plan to age 85

While the income advantage for the All-Asset Plan continues for the early retirement years, most of that tax advantage reverses itself at age 85 when certain tax breaks end. Using the same methodology as above, the tax rate goes up as the tax-deferred benefits end.

However, the income amounts go up as well, particularly QLAC, and thus there’s more income from that source — again pushing out the time for withdrawals.

At 85, the All-Asset Plan develops income of $238,000 and an estimated tax rate of 17.1%. The traditional investment-only plan income at 85 is $200,000 with an 18.5% estimated tax rate.

In the All-Asset Plan, we also provide for QLAC reserve income to pay for either the higher deductible expenses, taxes or both.

Tax analysis of legacy savings

Most of the tax attention above has appropriately been on income, particularly in the early retirement years. However, the amount paid out at passing (legacy), should get your attention as follows:

- Housing wealth. Step-up in basis of the value of the original home at passing

- Sale of house. Tax paid at sale, with some significant deductions

- Personal savings. Step-up in basis at passing

- Rollover IRA. Taxable at 100%

- Roth IRA. Not taxable

As we’ve written about before, aging in place — if it can avoid the sale of your house — can be a huge tax benefit.

Comparison of an All-Asset Plan to traditional investment-only

To put both the income and legacy elements together, we use the ROI as a measure of the economic return, considering both before- and after-tax income and legacy. Here’s the summary between all-assets and investment-only planning.

(Image credit: Courtesy of Jerry Golden)

In its simplest terms, you can save money when you take into account how taxes affect your retirement. Bottom line, the tax-cost advantage of an All-Asset Plan vs a traditional investment-only plan as measured here is .7%. That seems small, but not when compared with, say, advisory fees in the .5% to 1% range.

Housing wealth, personal savings and even Social Security benefits offer potential tax deferrals and savings. When creating a retirement plan, think about other tax benefits, such as deferring certain taxable events.

The tax code offers certain tax breaks that can improve your retirement outcomes. It’s up to me and others in the advisory space to point you to these advantages. As a next step, visit Go2Income, answer a few questions about your current income and future needs and start creating your own plan to grow your retirement income and liquid savings.