This Week

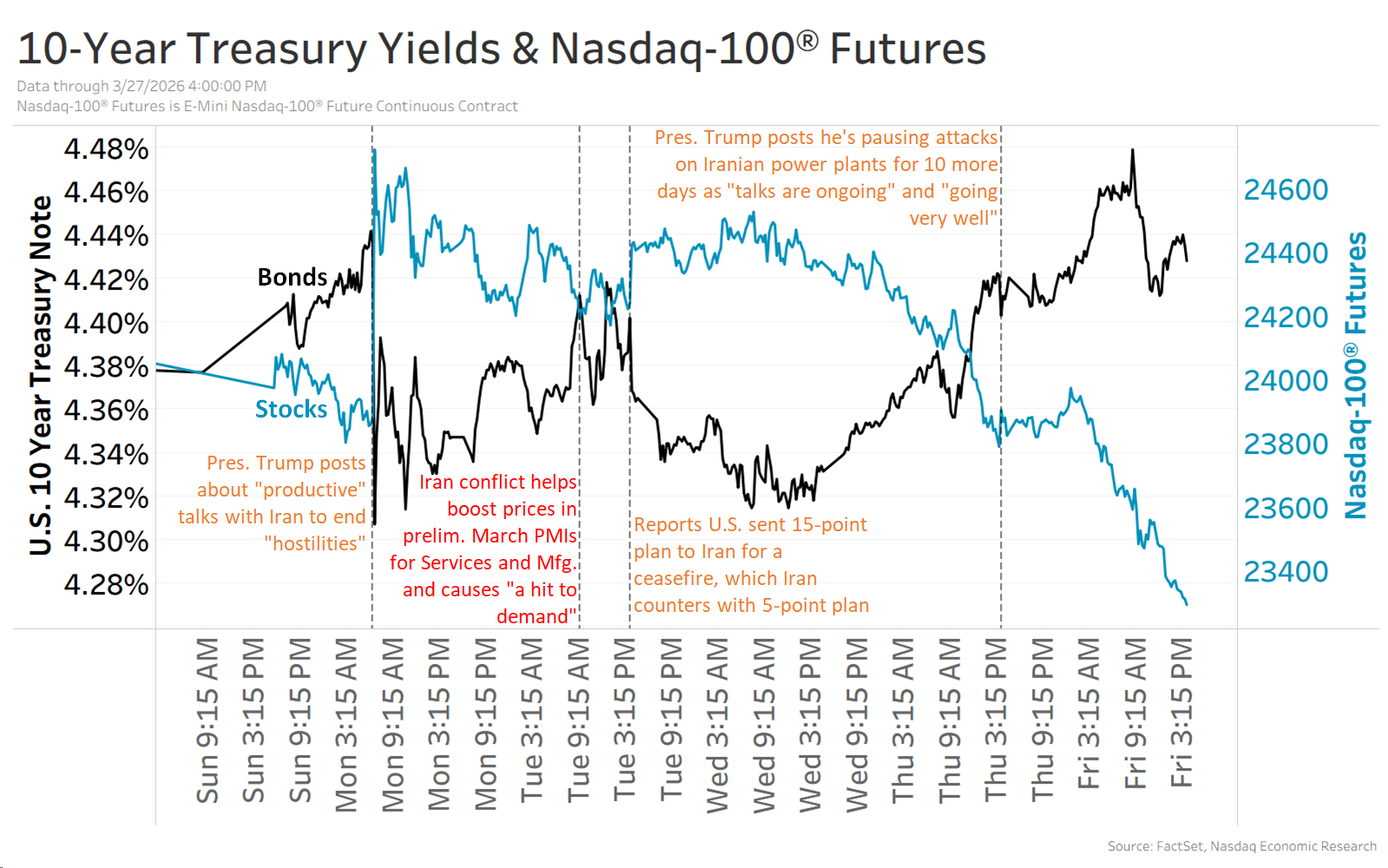

Once again, developments in the Iran conflict drove markets, and economic data started to capture the impact of the conflict.

In positive news, this week saw negotiations for a ceasefire begin:

- Monday: President Trump posted that the U.S. and Iran “”have had… very good and productive conversations regarding a… resolution of hostilities,” which Iran later denied.

- Tuesday: The U.S. sent a 15-point plan to Iran for a ceasefire, which Iran rejected.

- Wednesday: Iran counters with a five-point plan for a ceasefire, including reparations and Iranian control of the Strait of Hormuz.

- Thursday: President Trump posts that he’s pausing attacks on Iranian power plants for another 10 days to April 6 as “talks are ongoing and… going very well.”

While the sides appear far apart, these early-stage negotiations were seen as something of a positive, helping push Brent oil prices off their high of $119 per barrel to under $115 now.

Those higher oil prices are starting to show up in economic data, with the preliminary March S&P PMIs seeing input and output prices rising for Manufacturing and Services, and companies noting “a hit to demand from the additional uncertainty and cost-of-living impact generated by the conflict.”

Despite these initial negotiations, there’s no end in sight for the conflict, contributing to a 3% drop in the Nasdaq-100® this week, pushing it into correction (at least 10% off its high), and a 5 basis point increase in 10-year Treasury yields to over 4.4%.

Next Week

Here are the top events I’m watching next week:

- Tuesday: JOLTS Job Openings (Feb.)

- Wednesday: Retail Sales (Feb.), ISM and S&P Manufacturing PMIs (Mar.)

- Thursday: Jobless Claims

- Friday: Nonfarm Jobs Report (Mar.), ISM and S&P Services PMIs (Mar.)