Link to Report: Macro Volatility Digest

WHAT STANDS OUT:

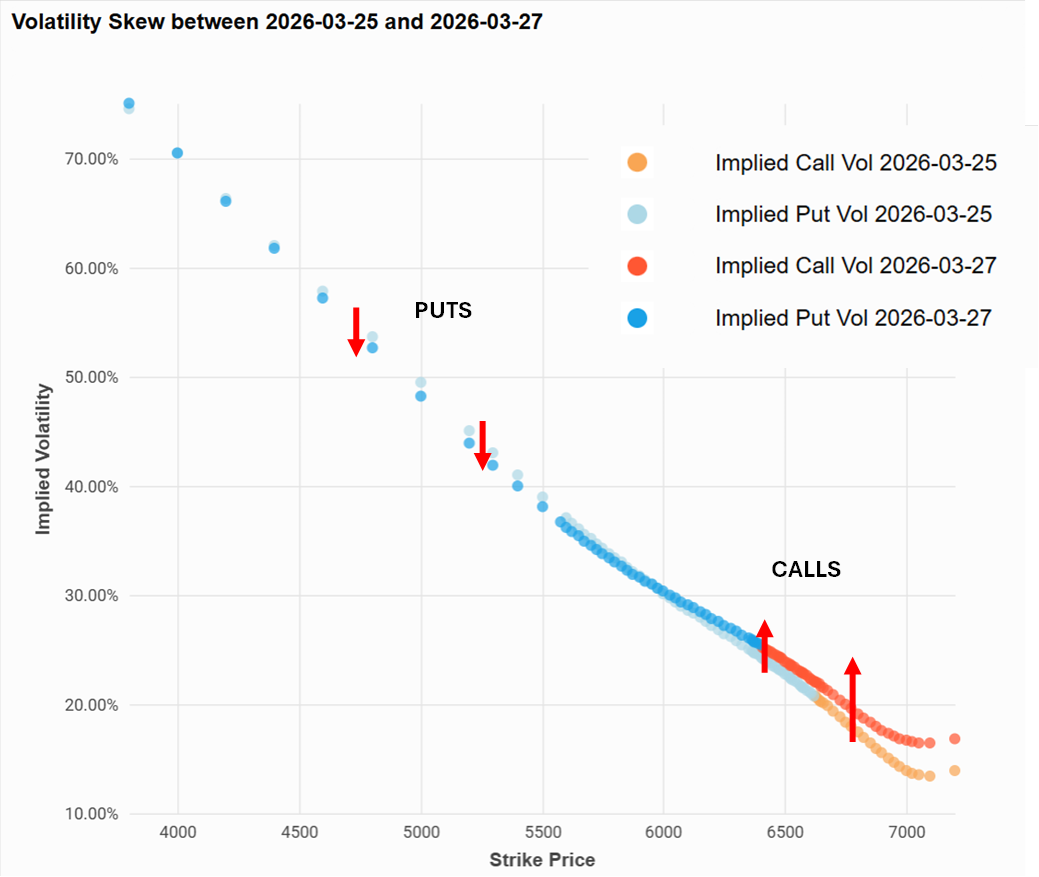

- The VIX® Index jumped 4.3 pts last week to 31%, ending the week at its highest level since last April’s sell-off. However, there’s been very little panic in the options market. Even when SPX Index fell 3.4% on Thu/Fri, the bid to volatility came from the upside rather than downside as investors positioned for a potential rebound (aka the “TACO Trade”). In fact, SPX put skew and put convexity both declined as investors used the pullback to monetize existing hedges. SPX 1M put skew has now fallen to the 2nd percentile low over the past year.

- Instead, we saw call demand pick up going into the weekend, adding almost 2 pts to the 5.7 pts increase in the VIX Index on Thu/Fri. See chart below. The optimism in the equity options market contrasts with the caution we’re seeing in the cross-asset vol markets, with oil options signaling potentially an extended period of supply disruption and the credit market starting to price in a more severe growth slowdown.

- Within equities, EM countries are bearing the brunt of the energy shock, with EEM 1M implied volatility nearing its “Liberation Day” high of 42% already (vs. the VIX Index which is still 20+ pts below its Apr’25 peak). The EEM-SPX 1M implied volatility spread widened to a 10-year high of 16% last week.

Chart: SPX Call Demand Jumps on TACO Optimism

Source: Cboe