2025 was a year of changing market dynamics, and Cboe’s U.S. Cash Equities team evolved with it, continuing to deliver customer-driven solutions and providing insightful analysis. Read on for a review of the key trends from 2025, Cboe’s accomplishments and look ahead to what’s next for 2026.

Key Takeaways

1. Record Growth Across U.S. Equities Markets

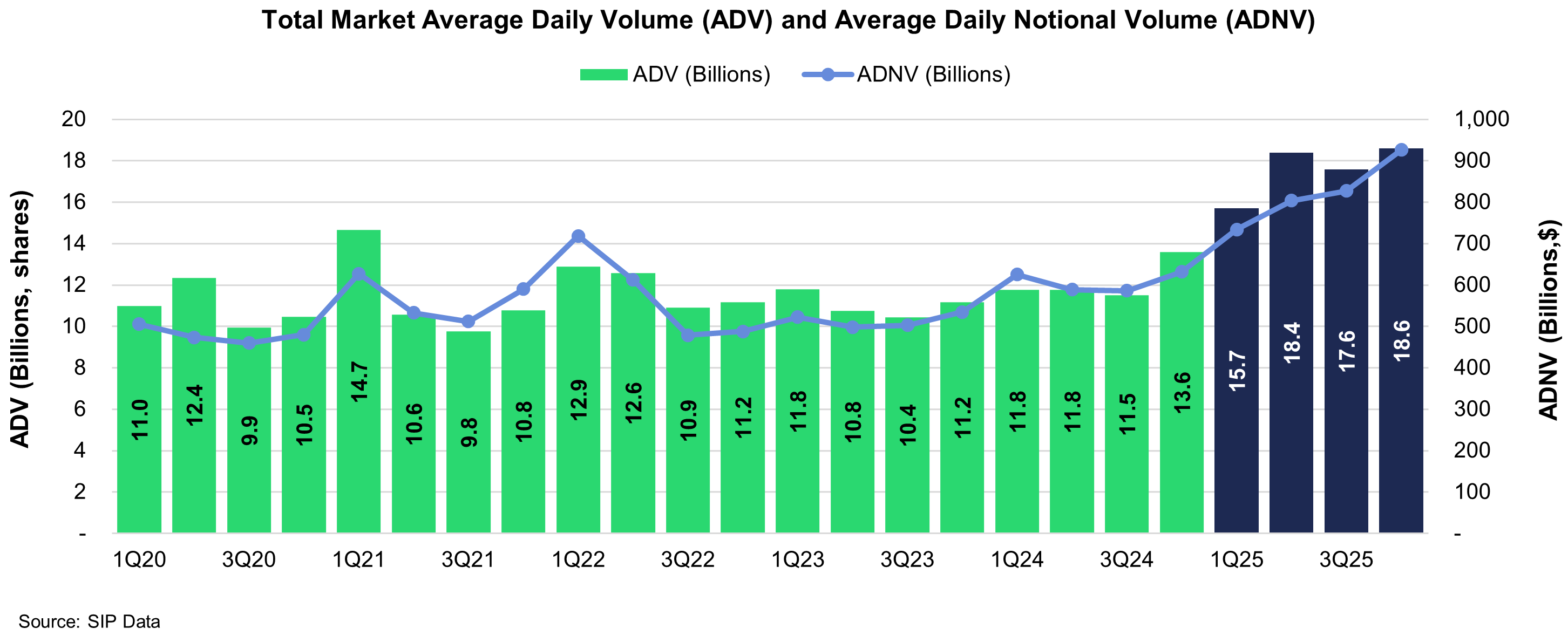

Industry wide, U.S. equities volumes reached record levels in 2025, with average daily volume increasing 44.6% year-over-year to 17.6 billion shares and average daily notional value rising 43.3%, to $1.1 trillion. This growth was accompanied by a shift to off-exchange trading, with Trade Reporting Facility (TRF) market share increasing 361 basis points to 50.6% of Total Consolidated Volume, marking the first time off-exchange trading exceeded half of all U.S. equities volume.

2. Strong Performance and Innovation in Cboe Premium Products

Cboe’s premium products demonstrated significant growth in 2025. Retail Price Improvement (RPI) on BYX grew 68% year-over-year to 2.8 million shares ADV, BYX Periodic Auctions ADV doubled (+109%), and Quote Depletion Protection (QDP) grew to 36.5 million shares ADV across EDGA and EDGX (+48%).

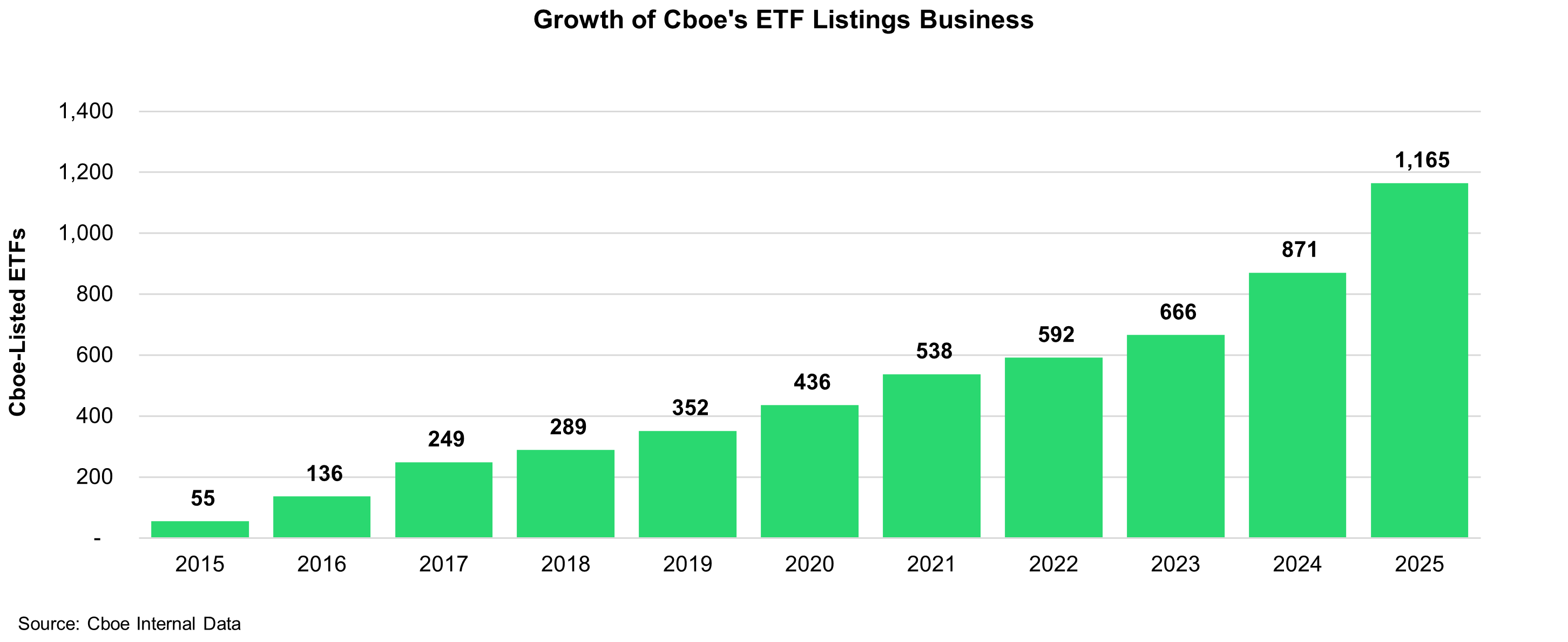

3. Record-Breaking Year for U.S. ETP Listings

Cboe’s ETF listings grew substantially in 2025, adding 394 new listings, the strongest year for Listings in the exchange’s history. The exchange solidified its position as the dominant venue for defined outcome products, now listing 85% of all outcome-based ETFs representing 94% of assets under management (AUM) in the category, while capturing approximately 60% of derivative-based product launches.

4. Transformational Changes Ahead in 2026

The market structure landscape is poised for significant evolution with the implementation of the Securities Exchange Commission’s (SEC)’s tick size and access fee amendments, ongoing Rule 611 discussions, and the anticipated December 2026 launch of extended trading hours. Cboe plans to introduce Enhanced Retail Price Improvement (RPI) on BYX and looks to expand the RPI program to EDGX, while leveraging its global infrastructure and proven near-24×5 capabilities in derivatives markets to lead the transition to 23×5 equities trading hours.

Read a detailed review of 2025 accomplishments for Cboe’s U.S. and Canadian Cash Equities businesses below.

Market Trends and Observations

Continued Strength in Equities Volume

U.S. equities volumes have grown over the past three years and remained elevated in 2025, achieving a new higher level of normalcy across the industry. Growing access and interest in the U.S. equities market, as well as domestic and international events contributed to increased volume traded during the year. In 2025, average daily volume (ADV) increased 44.6% year-over-year to 17.6 billion shares. U.S. equities notional value traded have followed a similar trend, with U.S. equities average daily notional value (ADNV) increasing 43.3% year-over-year to $1.1 trillion. U.S. equity markets reached a 2025 peak of 30.98 billion shares and $1.86 trillion notional value on April 9, 2025. April 9 marked the best one-gain day for the S&P 500 Index since October 2008 during the Great Recession, driven by President Trump’s announcement of a 90-day pause on most of the tariffs that went into effect on April 2, 2025. The Dow Jones Industrial Average and the Nasdaq Composite also experienced significant gains on April 9.

Growth in Dark Trading Volumes

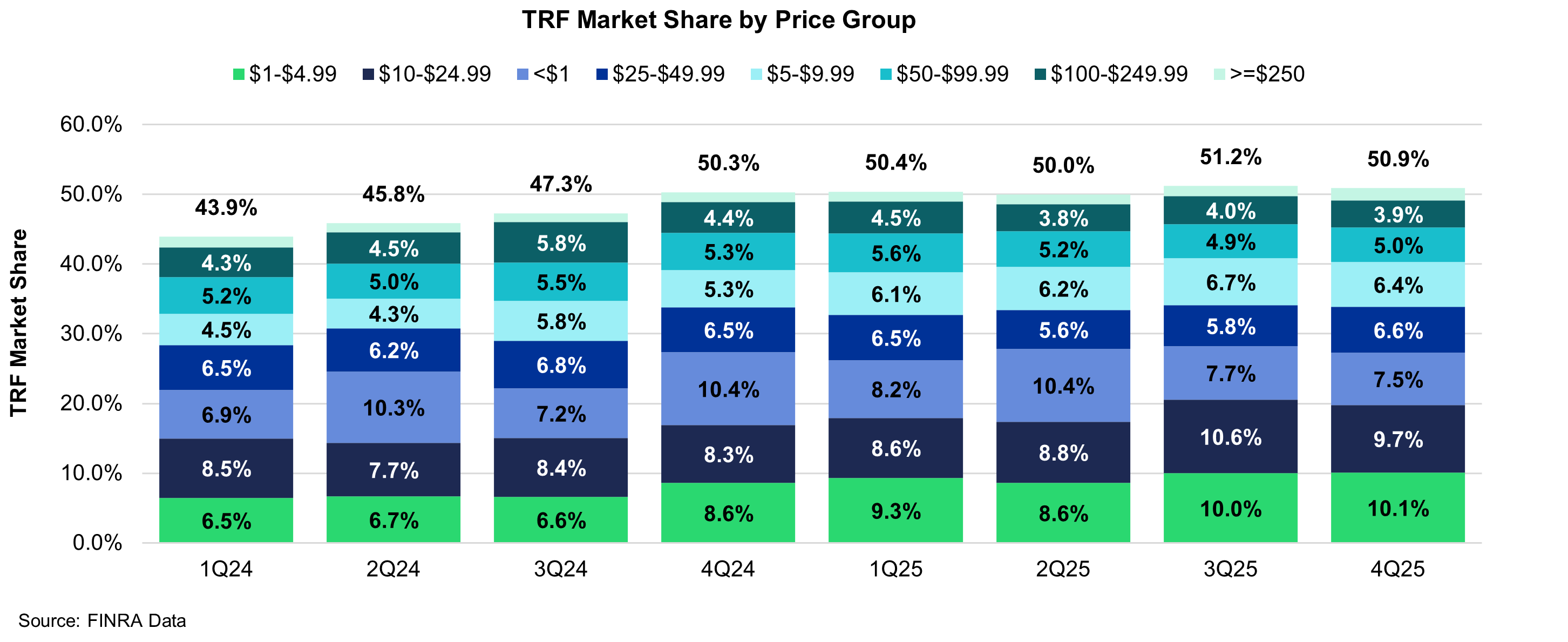

The rise in equities Total Consolidated Volume (TCV) over the past two years is correlated with increased market fragmentation, as trading activity has dispersed across multiple venues and shifted significantly toward off-exchange platforms. In 2025, off-exchange trading as measured by Trade Reporting Facility (TRF) market share increased 361 basis points (bps) to 50.6% of TCV. During the year, 18.7% of TRF volume occurred on Alternative Trading System (ATS) platforms and 81.3% through Principal Dealers. While sub-dollar securities liquidity has historically been the biggest driver of off-exchange trading, as seen in Figure 2 below, 2025 TRF market share gains were driven by securities priced between $1 and $4.99, as well as securities priced between $10 and $24.99. TRF market share in sub-dollar securities declined 40 bps in 2025 from the prior year.

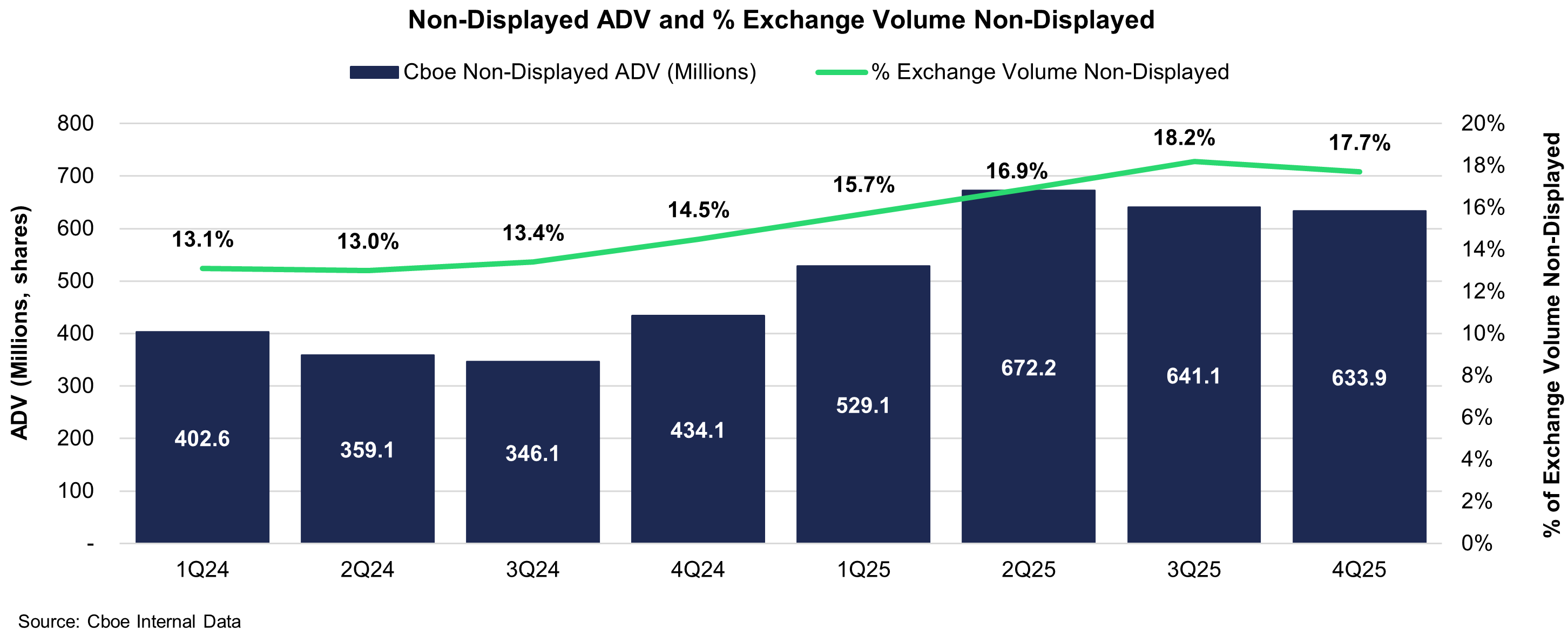

In November 2025, Cboe’s Equities Execution Consulting team published an analysis of dark trading volumes, “The Hidden Advantage: Cboe’s Premium Products In The Era Of Non-Displayed Trading,” which highlighted the multi-year trend that emphasizes growing interest in dark, or non-displayed execution. In addition to growth in off-exchange volumes, Cboe observed growth in on-exchange non-displayed volumes on its trading platforms alongside off-exchange growth. In 2025, 17.2% of volume executed on Cboe’s venues was non-displayed.

Retail and Premarket

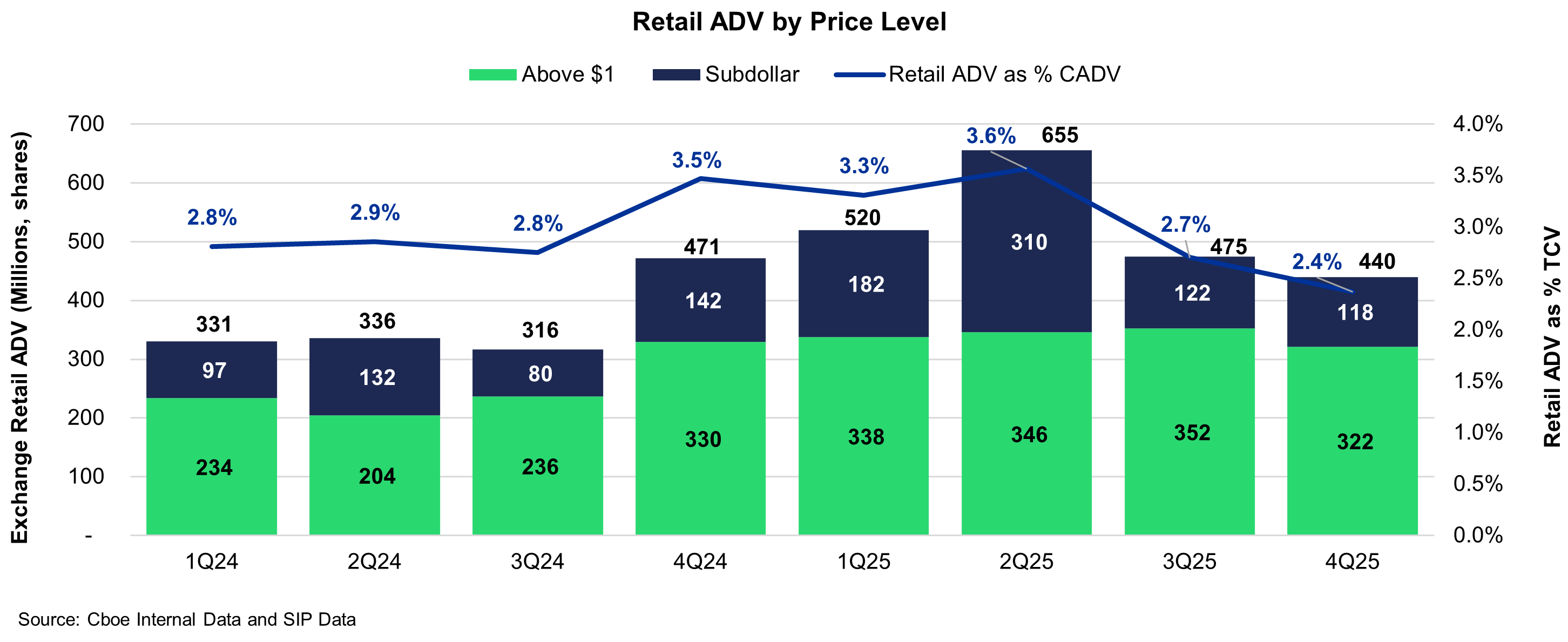

With volumes skyrocketing during the second quarter of the year, retail-attested trading volumes on Cboe have remained elevated in 2025 compared to 2024. Retail-attested ADV on Cboe’s exchanges increased 47.3% year-over-year, representing 3.2% of TCV. This increase was primarily driven by a 61.4% increase in sub-dollar retail ADV, while retail volume priced above $1 also increased 35.0% on Cboe’s venues. Specifically, Cboe EDGX® Equities Exchange (EDGX) retail ADV increased 51.3% year-over-year, representing 30.4% of EDGX volume, driven by increases in retail ADV priced below and above $1 of 64.9% and 38.4%, respectively.

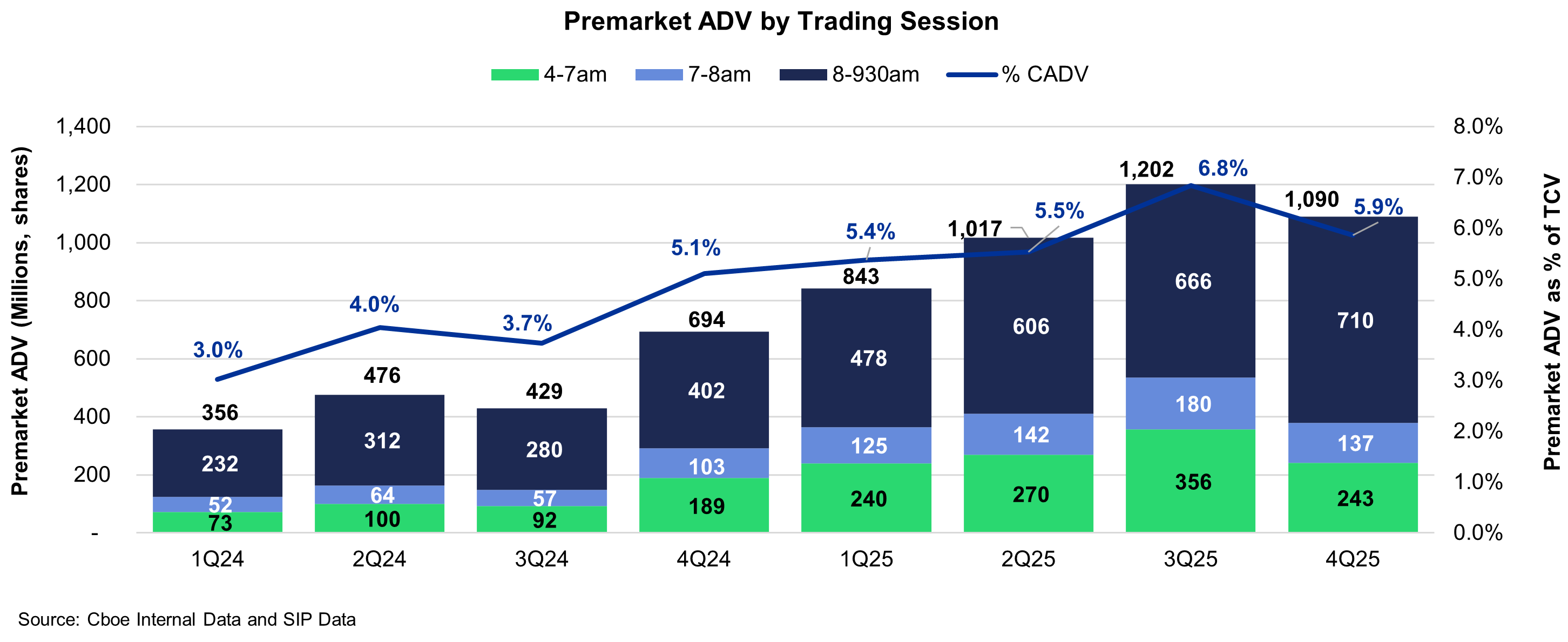

Growth in pre-market volume has outpaced the growth in retail-attested volume. In 2025, pre-market volume increased 111% year-over-year to 5.91% of TCV. Pre-market ADV increased more than 100% year-over-year, with 59.3% of pre-market trading volume transacting during the session between 8 am and 9:30 am.

U.S. Equities Product Updates

Cboe Premium Products

Retail Price Improvement

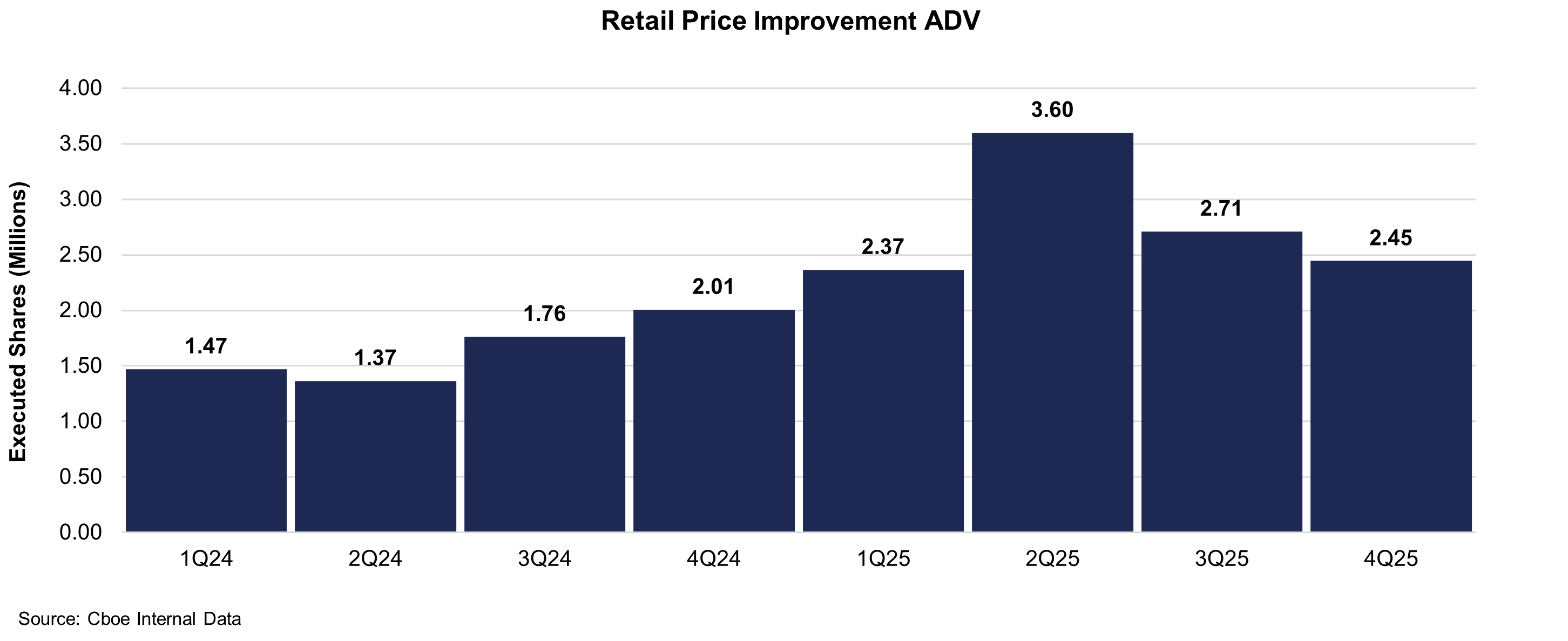

Retail Price Improvement (RPI) on Cboe’s BYX® Equities Exchange (BYX) grew 68% year-over-year, with a total of 695.2 million shares in RPI Orders executed. RPI enables Retail Member Organizations (RMOs) to potentially obtain price improvement supplied by liquidity providers in $0.001 increments better than the National Best Bid or Offer (NBBO). RMOs also have an opportunity to earn enhanced rebates when interacting with RPI Orders, which may result in an RMO receiving both price improvement from the executions as well as from the enhanced rebates. For liquidity providers, RPI Orders provide continuous access to retail flow that is generally preferred over non-retail flow. Liquidity providers can passively capture marketable retail demand throughout the trading day, offering an efficient alternative to aggressive liquidity-seeking strategies, while also receiving a lower fee for adding liquidity to BYX.

RPI volumes were strong during the second quarter, reaching 3.6 million ADV. During the second half of the year, RPI volumes settled at an elevated average of 2.6 million shares per day.

Periodic Auction

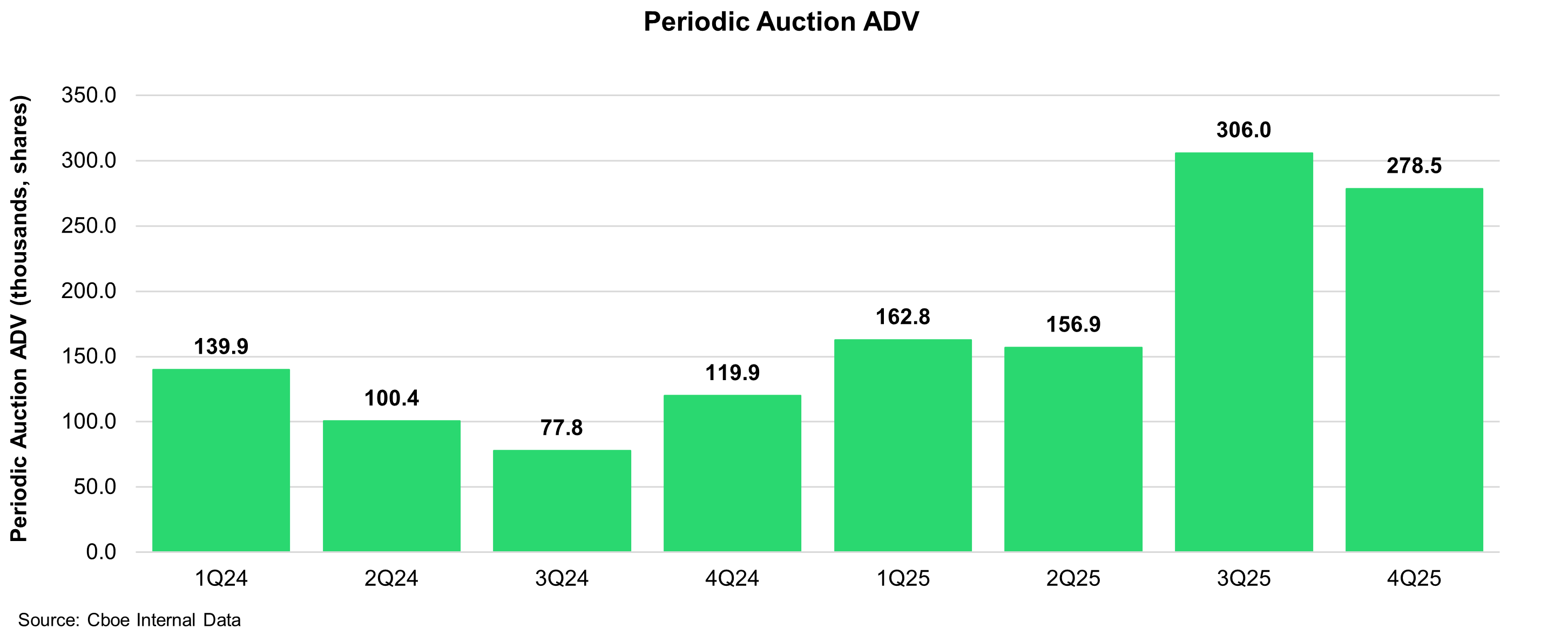

Periodic Auctions (PA) on Cboe’s BYX exchange offer an on-exchange model of sourcing size seamlessly while minimizing adverse selection. PA offers enhanced trade outcomes and provides the best markout performance compared to both displayed and non-displayed executions on BYX, with flat to positive markouts from 1 millisecond to 1 second after the trade[1]. For more details, see the analysis Cboe published in July 2025 of the unique liquidity-sourcing opportunity with minimal market impact as offered by Cboe’s Periodic Auctions and reach out to your account manager to receive missed opportunities by symbol in Periodic Auctions. Periodic Auction volume has doubled in 2025 from 2024, increasing by 109% year over year. Growth is expected to continue in 2026 after a strong second half of 2025, with new members connected and deploying PA to liquidity sourcing strategies.

Quote Depletion Protection (QDP)

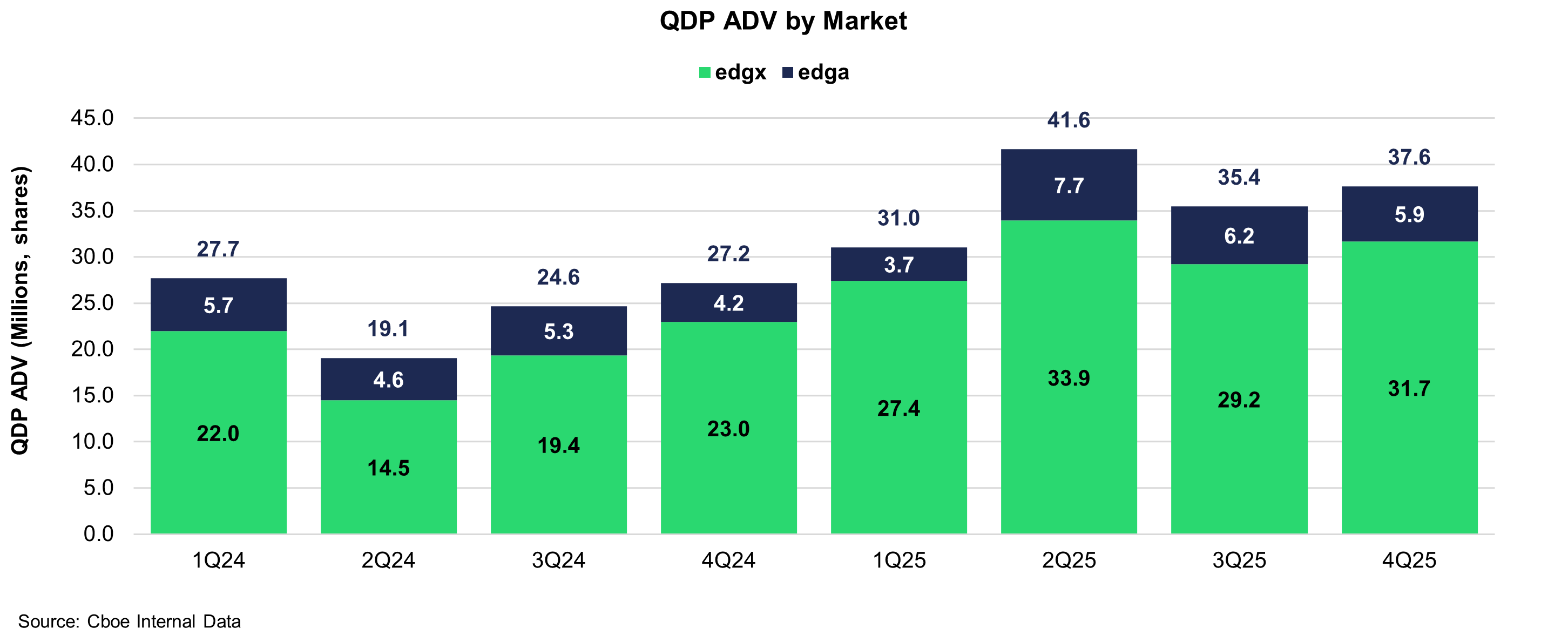

QDP enhances Midpoint Discretionary Orders (MDOs) by providing a unique layer of protection against adverse selection, ultimately driving better trading outcomes. Quote Depletion Protection (QDP) disables the discretionary range of MDOs for a short period of time to prevent the execution of trades at prices more aggressively than their ranked price. Available on Cboe’s EDGA and EDGX exchanges, QDP ADV was 5.9 million shares on EDGA and 30.6 million shares on EDGX in 2025, an increase of +48% year-over-year. QDP is heavily used on high volatility days, such as April 9, 2025, where QDP traded 101 million shares.

U.S. ETP Listings

Cboe achieved exceptional growth in ETF listings during 2025, adding 351 new listings and welcoming 43 transfers for a total of 394 new listings — the strongest year in Cboe’s history. The asset class composition reflected evolving market demand, with outcome-based ETFs leading at 128 listings, followed by 117 single-stock ETFs. The remainder of the new ETF listings were comprised of crypto, commodities, fixed income and international equity ETFs. Allianz’s transfer of 34 ETFs to Cboe was a defining moment of 2025. As one of the largest exchange transfers ever executed, it solidified Cboe’s position as the dominant venue for defined outcome products. Cboe now lists 85% of all outcome-based ETFs, representing 94% of AUM in the category. The exchange also expanded its issuer ecosystem by onboarding 30 new ETF sponsors throughout the year.

The 2025 listings landscape underscored a decisive industry shift toward derivatives-based innovation, with approximately 50% of all U.S. ETF launches incorporating options, futures or other derivatives strategies. Cboe captured this trend at an even higher rate, with roughly 60% of its new listings being derivative-based products, reflecting the exchange’s strength in structured and alternatives-focused ETFs.

Recognizing the diverse liquidity needs across asset classes, Cboe unveiled a reimagined Lead Market Maker (LMM) program in the fourth quarter that tailors quoting requirements to the specific characteristics of each ETF category, from outcome-based and single-stock products to traditional equity and fixed income funds. This differentiated approach positions Cboe to strengthen liquidity and market quality across today’s diverse strategies and provide issuers and market makers with a more flexible, efficient market structure heading into 2026.

What’s Next in 2026?

Tick Sizes, Access Fees, and Transparency of Better Priced Orders

On September 18, 2024, the Securities and Exchange Commission (SEC) approved proposed amendments affecting tick sizes, access fees and transparency of better priced orders. The final rule established a second minimum tick size, or price increment, for securities priced above $1, reduced the access fee caps, ensured that all fees and rebates are determinable at the time of trade execution and accelerated the implementation time for round lot definitions and dissemination of odd-lot information.

On December 12, 2024, the SEC granted a motion to stay the implementation of revised tick sizes and access fees. The stay did not affect the changes related to round lots, odd lots and fee transparency. The round lot changes were implemented on November 3, 2025. The fee transparency changes will be implemented on February 2, 2026. The SEC announced on October 31, 2025, that the effective date of the tick size and access fee changes is now the first business day of November 2026.

Rule 611 of Regulation NMS

The SEC hosted two roundtables on September 18, 2025, and December 16, 2025, which discussed Rule 611 of Regulation National Market System (Reg NMS), along with associated rules and regulatory requirements. Rule 611 of Reg NMS forbids trade-throughs in NMS stocks, protecting investors by prohibiting national securities exchanges from executing orders at trade prices worse than the best available prices displayed by other exchanges. Cboe published comment letters ahead of both the first and second SEC roundtables discussing Rule 611. In these letters, Cboe encouraged the SEC to approach any updates to Rule 611 with care, emphasizing the importance of maintaining a reliable NBBO, avoiding unintended market‑structure disruptions and recognizing the distinct dynamics of the options market. Additionally, Cboe posited that any reforms should be evaluated holistically and with an emphasis on simplicity, particularly given today’s evolving trading landscape and the nuanced realities of exchange participation.

23×5 Trading

On December 19, 2025, the Operating Committee of the Securities Information Processors (SIPs) announced the submission of a Plan Amendment to the SEC to extend SIP operating hours to accommodate overnight trading. As previously announced, the SIPs plan for hours of operation is designed to be as close to 24 hour trading as technically possible. The new extended trading hours are anticipated in December 2026 or early 2027, pending SEC review and industry readiness. As announced in February 2025, Cboe plans to offer 23-hour, five-days-a-week (23×5) trading for U.S. equities on its Cboe EDGX Equities Exchange (EDGX), subject to regulatory review and industry developments, including the readiness of the SIP. Cboe already offers near 24×5 Global Trading Hours (GTH) for multiple proprietary products, including VIX® futures and SPX and VIX options, and continues to expand this capability with the launch of nearly 24-hour trading for Russell 2000 Options starting February 9, 2026. Cboe’s existing model for around-the-clock derivatives trading serves as the blueprint for expanded equities trading hours. Not only is Cboe already equipped with the technological capabilities to offer 23×5 trading, Cboe is also especially well positioned to support 23×5 trading with our locally optimized, globally consistent approach.

New Products

Enhanced RPI

The SEC approved Cboe’s proposal requesting the addition of an Enhanced Retail Price Improvement (ERPI) order type to the RPI Program. Like standard RPI Orders, ERPI Orders consist of non-displayed interest on the exchange that is eligible to execute against contra-side retail orders in $0.001 increments and is ranked at its limit price. However, an ERPI Order also includes a Step-Up Range Instruction (i.e., a maximum execution price for buy orders and a minimum execution price for sell orders) at which the ERPI Order is willing to execute. As a result, ERPI Orders will allow retail liquidity providers to post orders at a specific limit price, but at the same time be positioned to earn price priority if the associated Step-Up Range Instruction provides a meaningful amount of price improvement as compared to other resting orders on the BYX book. Enhanced RPI is expected to be available on BYX on January 30, 2026.

RPI for EDGX (pending regulatory approval)

Cboe is planning to introduce an RPI Program to EDGX, pending SEC approval. The EDGX RPI Program will be structured like the BYX RPI Program wherein liquidity providers can offer price improvement exclusively to retail-attested orders, but the EDGX RPI Program will also offer additional functionality allowing RPI liquidity providers to use the Midpoint Peg instruction. EDGX RPI will not support the Enhanced RPI Order type.

Non-Displayed Day ISO Order Type (pending regulatory approval)

Cboe is looking to add the ability to include an Intermarket Sweep Order (ISO) instruction on non-displayed orders with a time-in-force other than Immediate-or-Cancel (IOC) across all Cboe US Equities exchanges, pending SEC approval. If approved, Cboe exchanges will be able to accept and process non-displayed orders with a time-in-force other than IOC containing an ISO instruction in a similar manner to how displayed ISOs with a time-in-force other than IOC are processed.

Looking Ahead to 2026

As we move into 2026, we remain committed to building on last year’s momentum by broadening our innovative product offerings and deepening our analysis of evolving market trends. We invite you to explore our latest perspectives on Cboe Insights, where our goal is to support you, our valued clients, with key insights to help inform your trading decisions.

Thank you for your continued trust and thoughtful feedback. We greatly value your partnership and will keep striving to deliver meaningful, forward-looking solutions in the year ahead. As always, please feel free to reach out to any member of our team with questions.

There are important risks associated with transacting in any of the Cboe Company products discussed here. Before engaging in any transactions in those products, it is important for market participants to carefully review the disclosures and disclaimers contained at: https://www.cboe.com/us_disclaimers/. These products are complex and are suitable only for sophisticated market participants. In certain jurisdictions, Cboe Company products are only permitted for investment professionals, certified sophisticated investors, or high net worth corporations and associations. These products involve the risk of loss, which can be substantial and, depending on the type of product, can exceed the amount of money deposited in establishing the position. Market participants should put at risk only funds that they can afford to lose without affecting their lifestyle. © 2025 Cboe Exchange, Inc. All Rights Reserved.