Living in Idaho might feel and sound like an affordable idea, but Idaho debt relief is becoming a very significant service as Idahoans are challenged by rising housing expenses, irregular incomes, and unexpected bills. Whether in Boise, Idaho, or in other parts of the state, the availability of financial advice can be an issue.

For a comprehensive overview of national options, see our Debt Relief Overview.

Why Is Debt Relief Unique in Idaho?

The debt situation in Idaho is not the same as in coastal or expensive states. Even though the overall costs might be lower, the residents still have to deal with some issues, such as:

- Rural and urban access — Online or remote programs are mostly the only way for residents living beyond Boise or Nampa to get access to the services.

- Seasonal employment — There are income fluctuations due to agricultural and tourist jobs.

- Medical and emergency expenses — Limited access to hospitals could cause a patient to incur higher out-of-pocket costs.

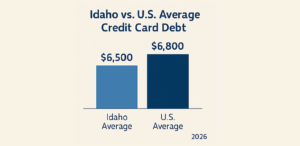

An average Idaho adult holds about $6,500 as credit card debt, and household debt comprising mortgages and personal loans has shown a steady rise over the last five years.

Information taken from Forbes

What Types of Idaho Debt Relief Programs Are Available?

Understanding the types of programs helps Idaho residents choose the right option:

Debt Settlement

Negotiates your unsecured debt for less than what is owed, often used for credit cards, medical bills, and personal loans. Accounts are managed online, and monthly payments typically last 24–48 months.

Debt Management Plans (DMPs)

Offered by nonprofit agencies, DMPs consolidate payments and lower interest rates. They are ideal for residents with a steady income but multiple small-to-mid debt balances. Rural residents may rely on online sessions rather than in-person meetings.

Debt Consolidation Loans

Combines multiple debts into one loan with a lower interest rate. Best for residents with good credit and financial discipline. Local lenders in Meridian or Twin Falls may offer competitive products.

Credit Counseling

Provides education and budgeting guidance, particularly useful for smaller balances. Nonprofit agencies can help Idaho residents plan repayment and avoid future debt traps.

Bankruptcy (Last Resort)

Legal mechanism to discharge debts, but comes with a long-term credit impact. Residents should consult a licensed Idaho attorney before pursuing.

For a detailed comparison of national debt solutions, check out the Top 21 Debt Settlement Companies.

Who Qualifies for Idaho Debt Relief Programs?

Curious if debt relief fits your situation? See if you qualify for a customized plan with New Era’s settlement program using their free assessment tool.

Explore a Free Consultation

Top Idaho Debt Relief Companies Compared

Choosing the right provider significantly impacts your results. The following companies offer programs for Idaho residents:

Idaho Debt Relief Companies Comparison

| Company | Best For | Minimum Debt | Fees | Serves Idaho |

| New Era Debt Solutions | Personalized settlement for large unsecured debt | $10,000 | Performance-based | Nationwide |

| Century Support Services | Nonprofit credit counseling & debt management | None / Low | Counseling & DMP fees | Licensed in Idaho |

| ClearOne Advantage | Structured repayment plans & debt management | $5,000 | Performance-based | Nationwide |

| Money Management International | National nonprofit counseling & DMPs | None / Low | Counseling & DMP fees | Online / Idaho |

| Accredited Debt Relief | Major unsecured debt settlement | $7,500 | Performance-based | Nationwide |

Highlighted Company Insights

New Era Debt Solutions — Best for people who reside in Idaho and have a high amount of credit card debt or personal loan debt. Their negotiation methods can lower balances remotely to help rural clients.

Thinking about choosing New Era for Debt support? Explore our expert review to learn what they offer and if they’re the right fit.

Century Support Services — An Idaho-licensed nonprofit that provides credit counseling and DMPs with reduced interest rates instead of aggressive settlements.

ClearOne Advantage — Offers structured repayment plans, along with flexibility in finding solutions for mixed unsecured debt, so the client can avoid bankruptcy when possible.

Money Management International — National nonprofit specializing in credit counseling and DMPs, with the added value of online accessibility to assure participation by even rural Idaho residents.

Accredited Debt Relief — Major unsecured debt settlement is the focus, with performance-based fees. It is nationwide, ensuring clients have wide access to a broad creditor network.

For additional context on debt settlement providers, see our JG Wentworth Debt Relief Review.

How to Choose the Right Idaho Debt Relief Program

Before signing up, local residents ought to think about:

- Overall unsecured debt sum — Large amounts of debt might require settlements; lesser amounts could be managed through DMPs or credit counseling.

- Monthly affordability — Most programs last 24–48 months.

- Credit impact — A few programs might lower the credit score in the short run.

- Provider reputation — Check customer feedback and verify that the provider is legally compliant.

- Remote access — A must-have for people living in the countryside of Idaho.

If you need further help, our Reprise Financial Review can help in comparisons of program types, fees, and results.

Common Mistakes Idaho Residents Make With Debt Relief

- Enrolling with insufficient debt to justify the program fees

- Looking forward to immediate credit score improvements

- Turning a blind eye to the contracts or disclosures signed

- Still using credit cards while being in the program

- Picking providers who don’t offer online accessibility

Tip: Rural Idaho residents should prioritize providers with robust internet and phone support.

Who Makes the Top Debt Settlement List in 2024?

Find and compare the best-rated companies to fit your situation — backed by reviews and ratings on CPI’s trusted list.

Check the 2024 Rankings & Free Guide

How Does Average Debt Vary Across Idaho Cities?

| City | Avg. Credit Card Debt | Avg. Mortgage Debt | Avg. Total Debt |

| Boise | $6,800 | $180,000 | $186,800 |

| Coeur d’Alene | $6,200 | $150,000 | $156,200 |

| Meridian | $7,000 | $175,000 | $182,000 |

FAQs — Idaho Debt Relief Programs Explained

How long does it usually take for Idaho debt relief programs to work?

The majority of Idaho debt relief programs have a duration of 2 to 4 years, which depends on factors such as the amount of your total debt, how cooperative your creditors are, and your monthly contributions. If you plan your financing properly, you can refer to the Debt Relief Overview information and avoid unnecessary waits.

Are debt relief Idaho services safe and legal for the locals?

Absolutely. All Idaho debt relief businesses are obligated to adhere to federal consumer protection laws. By picking a licensed, well-governed company, you are taking the first step toward financial security and will be assured that the program is run in an open manner.

Does my credit score get negatively affected if I go for Idaho debt relief programs?

Debt settlement might cause your credit score to fall a bit temporarily, but mostly, Idaho debt relief programs that are like DMPs or credit counseling don’t really cause any credit damage at all, other than barely. Keeping up with a payment schedule means your credit is protected over the long haul.

What level of indebtedness does one need to have to be eligible for Idaho debt relief?

Generally, a program requires a minimum of $7,500–$10,000 worth of unsecured debt. Nonprofits can still offer counseling to clients operating with smaller balances. Take advantage of your free assessments, such as See If You Qualify, to guide you in choosing the best program to repay effectively without taking on additional financial risks.

Where do we draw the line of bankruptcy as a solution for Idaho residents?

Bankruptcy is mostly considered a last-ditch solution. In fact, most Idaho debt relief programs offer structured alternatives that have a lower long-term negative impact on one’s credit. You should only consider legal remedies if you are totally overwhelmed with your debts.

Brandi Marcene is a financial writer and journalist with decades of experience writing about investing, personal finance, debt, and various economic news. Her writing has been published by several Fortune 500 companies, including Dell, SophisticatedInvestor, Haute, Audemars Piguet & Harry Winston.