By David Enna, Tipswatch.com

As the Federal Reserve continues on a path toward lower short-term interest rates, the bond market isn’t tagging along. Instead, yields on medium- and longer-term Treasurys have been increasing, not falling.

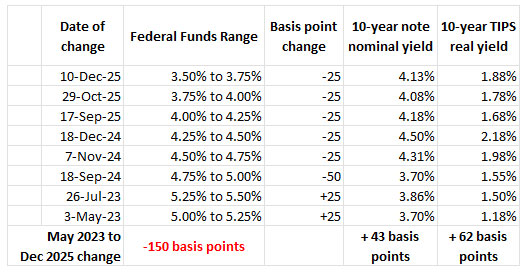

The Fed began its latest phase of rate-cutting on Sept. 17, 2025, and has now cut the federal funds rate by 75 basis points over the last four months. That has brought short-term rates down, but has had no effect in lowering longer-term rates:

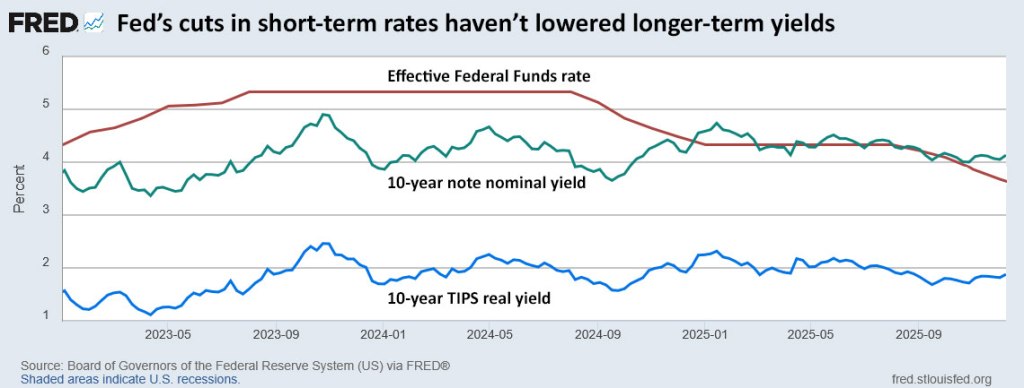

Here is a view of 10-year real and nominal Treasury yields over the last three years, during a time of 1) Fed rate increases, 2) then stability, 3) then cuts. Since September, both real and nominal 10-year real yields have remained relatively stable, even as the Federal Reserve was cutting short-term rates.

And this final chart shows that both 10-year nominal and real yields are up strongly since the Fed ended its rate-increasing cycle in mid-2023. The Federal Funds rate has fallen 150 basis points since May 2023, but both real and nominal 10-year yields are up, fairly dramatically.

Why is this important?

The market yield on the 10-year Treasury note is a key benchmark in the U.S. economy, forming the basis for mortgage rates and business loans. Normally, when the Fed cuts short-term rates, you’d expect to see longer-term yields move in that direction. That isn’t happening in 2025.

Why? One key reason is that the bond market sees U.S. deficits continuing to rise, possibly dramatically, over the next five years or longer. It’s a long-term trend, and it is escalating. When President Trump took office on Jan. 20, the U.S. government debt stood at $36.22 trillion. As of last week, that number was $38.39 trillion, according to the U.S. Treasury’s “Debt to the Penny” reports.

Another factor is inflation expectations. The Federal Reserve yesterday projected PCE inflation (which generally runs lower than headline CPI) to continue at 2.5% through 2026 before falling to 2.1% in 2027 and 2.0% in 2028. That looks like an overly optimistic forecast to me and the bond market seems to agree. The 5-year inflation breakeven rate closed Wednesday at 2.32%.

From a Bloomberg report on Dec. 7:

The bond market’s reaction to the Federal Reserve’s interest-rate cuts has been highly unusual. By some measures, a disconnect like this, with Treasury yields climbing as the central bank lowers rates, hasn’t been seen since the 1990s. …

But one thing is clear: the bond market isn’t buying President Donald Trump’s idea that faster rate cuts will send bond yields sliding down and, in turn, slash the rates on mortgages, credit cards and other types of loans.

Jim Bianco, president of Bianco Research, told Bloomberg the higher yields are a signal that bond traders are worried the Fed is cutting rates even as inflation remains stubbornly above its 2% target and the economy keeps defying recession fears.

“The market is really concerned about the policy,” said Bianco. “The concern is that the Fed has gone too far.” If the Fed continues to cut rates, he said, mortgage rates will go “vertical.”

And of course there is the issue of the Fed’s independence, which hangs over the bond market. Chairman Jay Powell will be gone in May, most likely replaced by Trump’s chief economist, Kevin Hassett, who has advocated for Trump’s policies on tariffs and lower interest rates. At this point, it looks like the Fed’s Open Market Committee is deeply divided over future rate-setting. That looks likely to continue.

The bond market is sending a message: The Fed can control short-term interest rates, but the market determines longer-term rates, unless the Fed launches another round of aggressive quantitative easing. (Opinion: that must not happen.)

So I would expect mid- to longer-term real and nominal yields to remain attractive into 2026, even as yields on savings accounts and money markets begin to fall.

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.