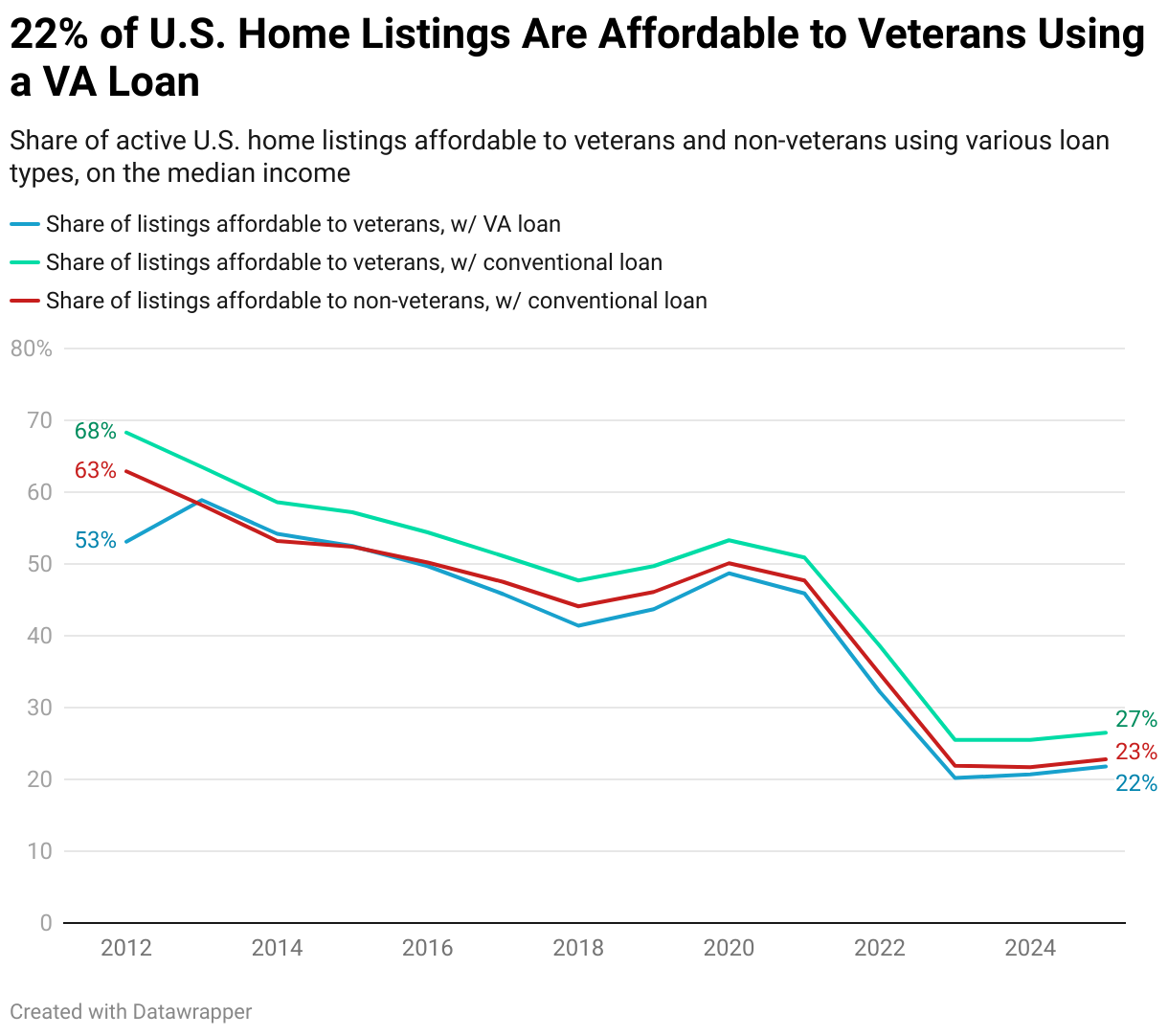

- 22% of U.S. home listings are affordable to the typical U.S. military veteran using a VA loan.

- Veterans–both those using VA loans and those using conventional loans–can afford slightly more home listings than they could have in 2023, when affordability was at an all-time low. Now, incomes are rising faster than housing payments.

- But veterans can afford half as many listings as they could have a decade ago, before the pandemic-driven homebuying frenzy.

- Veterans can afford more than half of homes for sale in Detroit and San Antonio, and almost no listings in expensive California metros.

Nationwide, just over one in five (21.8%) home listings are affordable to the typical U.S. military veteran using a VA loan, while 26.5% are affordable to the typical veteran using a conventional loan.

Affordability has improved slightly over the last two years. Just 20.2% of listings were affordable to the typical veteran using a VA loan in 2023, and 25.5% were affordable to veterans using a conventional loan, the lowest shares on record.

For comparison, a similar share (22.8%) of listings are affordable to the typical U.S. non-veteran household with a conventional loan. That’s a slight improvement from 2024’s low point, when 21.7% of listings were affordable for non-veterans.

This is from a Redfin analysis of housing affordability for veterans. It measures median household income for U.S. veterans and non-veterans, and the share of active listings each group is able to afford, based on the rule of thumb that a home is affordable if the estimated monthly mortgage payment is no more than 30% of the median monthly income. We included listings from January-September of 2012-2025. Please see the end of this report for more on methodology.

VA loans, which are insured by the U.S. government, are available to veterans, service members and their surviving spouses. They require little to no down payment. Here’s more info on how VA loans work, and here’s a list of common misconceptions about them. One benefit of VA loans is that they’re assumable; here’s what that means for veterans, homebuyers and sellers.

Homebuying affordability has improved marginally for both veterans and non-veterans over the last two years because monthly housing payments have declined, while incomes have risen:

- The average mortgage rate was 6.81% in 2023, and it is 6.66% today. Home-sale prices have flattened; the median U.S. sale price has posted a sub-2% year-over-year increase since April. The median monthly housing payment is lower now than it was two years ago.

- The median household income for veterans is an estimated $85,955 this year, up roughly 10% since 2023. For non-veterans, it is an estimated $81,078, also up roughly 10% over that period.

Veterans using VA loans are consistently able to afford fewer listings than homebuyers who take out conventional loans. Even though the typical veteran earns more than the typical non-veteran–and VA loans come with a slightly lower mortgage rate and no private mortgage insurance–90% of VA loan users make no down payment, which inflates monthly payments.

“VA loans provide a great opportunity for first-time veteran homebuyers to purchase a home without the substantial down payment that’s required of most buyers these days,” said Redfin Economist Grishma Bhattarai. “It allows them to get their foot in the homeownership door and start building equity, but it comes with the tradeoff of a bigger loan and higher monthly costs. That tradeoff is likely the reason why some veterans choose to take out a conventional loan and make a down payment, even if they qualify for a VA loan.”

Nationwide, 7.3% of mortgaged homebuyers used a VA loan in August. That’s a small share, but it’s up from 6.5% a year ago and it’s the highest share of any August in six years. More people are taking out VA loans because in today’s buyer’s market, more sellers are open to accepting buyers coming with no down payment.

Veterans Using a VA Loan Could Have Bought 53% of U.S. Listings in 2015, Before Housing Affordability Eroded

Veterans (and non-veterans) can afford far fewer listings than they could have a decade ago. A veteran using a VA loan could afford more than half (53%) of home listings nationwide in 2015, more than double the share they can afford today. A veteran using a conventional loan could afford roughly 57% of listings in 2015, and a non-veteran using a conventional loan could afford about 52%.

It has become much more difficult to afford a home because sale prices skyrocketed during the pandemic, then rising mortgage rates pushed monthly housing payments to new heights.

The hike in housing costs has far outpaced income increases over the last 10 years. The median U.S. home-sale price has roughly doubled over that period, with the biggest jump in 2021, when record-low mortgage rates and remote work caused a homebuying frenzy. The typical veteran’s household income has increased by 48% over that period, roughly half the rate of home prices. The typical non-veteran’s income has increased 54%.

Even with access to financial tools like VA loans, the typical veteran is priced out of many listings. A low-down-payment loan can only do so much when home prices and mortgage rates are elevated. The bright side is that homebuying affordability has started improving in parts of the country where home prices are declining, including several Florida metros, Phoenix, and Atlanta. And mortgage rates have come down from their peak, with the average 30-year fixed rate sitting near its lowest level in a year.

More Than Half of Listings Are Affordable to VA Borrowers in Detroit and San Antonio

Three in five (60%) home listings are affordable to a veteran using a VA loan in Detroit, more than any other major U.S. metro area. Next comes San Antonio, where more than half (53.4%) of listings are affordable. It’s followed by Cleveland (48.3%), Pittsburgh (43.6%) and Baltimore (42.7%).

The ranking is the same for veterans using conventional loans, though they can afford a slightly higher share of listings: In Detroit, 64.9% of listings are affordable to that group. Next are San Antonio (61.1%), Cleveland (53.3%), Baltimore (49.9%), and Pittsburgh (49.3%).

On the flip side, veterans can afford almost no home listings in California. In San Jose, Los Angeles and San Francisco, a veteran using a VA loan can afford less than 1% of for-sale homes, the smallest shares in the country. Next come San Diego and Anaheim, where they can afford roughly 2% of listings.

Using a conventional loan, veterans can afford 1% or fewer listings in San Jose and Los Angeles, 1.3% in San Francisco, 3.6% in San Diego, and 2.9% in Anaheim.

Veterans, like other homebuyers, can afford a far higher share of homes in places where homes are relatively affordable than in places where homes are expensive. The typical Detroit home sold for $215,000 in September, while the typical San Jose home sold for $1.6 million.

| Metro-Level Summary: Share of for-sale homes affordable on the median income, by various loan types

50 most populous U.S. metro areas |

|||

| U.S. metro area | Share of home listings affordable to veterans, w/ VA loan | Share of home listings affordable to veterans, w/ conventional loan | Share of home listings affordable to non-veterans, w/ conventional loan |

| Anaheim, CA | 2.2% | 2.9% | 3.6% |

| Atlanta, GA | 25.6% | 32.9% | 28.7% |

| Austin, TX | 19.2% | 26.0% | 24.2% |

| Baltimore, MD | 42.7% | 49.9% | 43.3% |

| Boston, MA | 4.0% | 5.5% | 9.7% |

| Charlotte, NC | 8.2% | 11.8% | 9.8% |

| Chicago, IL | 32.5% | 38.3% | 44.0% |

| Cincinnati, OH | 35.6% | 42.4% | 46.8% |

| Cleveland, OH | 48.3% | 53.3% | 54.5% |

| Columbus, OH | 33.3% | 39.6% | 37.2% |

| Dallas, TX | 29.8% | 37.4% | 29.3% |

| Denver, CO | 10.1% | 12.9% | 14.3% |

| Detroit, MI | 60.0% | 64.9% | 59.5% |

| Fort Lauderdale, FL | 31.2% | 34.3% | 28.1% |

| Fort Worth, TX | 33.8% | 43.7% | 27.3% |

| Houston, TX | 38.5% | 45.4% | 32.5% |

| Indianapolis, IN | 38.7% | 46.5% | 46.2% |

| Jacksonville, FL | 27.1% | 32.4% | 21.9% |

| Kansas City, MO | 32.3% | 39.1% | 40.2% |

| Las Vegas, NV | 11.6% | 14.5% | 10.3% |

| Los Angeles, CA | 0.7% | 1.0% | 1.0% |

| Miami, FL | 15.1% | 17.9% | 10.7% |

| Milwaukee, WI | 27.2% | 33.0% | 34.7% |

| Minneapolis, MN | 23.8% | 30.9% | 40.4% |

| Montgomery County, PA | 17.2% | 22.1% | 35.9% |

| Nashville, TN | 6.7% | 9.8% | 7.9% |

| Nassau County, NY | 5.2% | 6.4% | 11.7% |

| New Brunswick, NJ | 11.1% | 13.8% | 22.1% |

| New York, NY | 7.0% | 8.6% | 10.0% |

| Newark, NJ | 10.2% | 13.2% | 18.3% |

| Oakland, CA | 4.7% | 6.4% | 9.6% |

| Orlando, FL | 18.8% | 23.0% | 16.2% |

| Philadelphia, PA | 37.1% | 42.3% | 38.2% |

| Phoenix, AZ | 7.5% | 10.5% | 10.1% |

| Pittsburgh, PA | 43.6% | 49.3% | 55.5% |

| Portland, OR | 5.4% | 7.3% | 9.5% |

| Providence, RI | 5.2% | 7.0% | 9.7% |

| Riverside, CA | 5.9% | 8.0% | 6.4% |

| Sacramento, CA | 4.5% | 6.2% | 6.8% |

| San Antonio, TX | 53.4% | 61.1% | 34.9% |

| San Diego, CA | 2.1% | 3.6% | 2.0% |

| San Francisco, CA | 0.9% | 1.3% | 4.6% |

| San Jose, CA | 0.1% | 0.4% | 4.3% |

| Seattle, WA | 5.2% | 6.9% | 10.9% |

| St. Louis, MO | 39.3% | 44.2% | 48.6% |

| Tampa, FL | 19.2% | 24.1% | 18.4% |

| Virginia Beach, VA | 33.7% | 40.9% | 17.2% |

| Warren, MI | 37.3% | 43.4% | 48.9% |

| Washington, DC | 33.8% | 41.1% | 28.7% |

| West Palm Beach, FL | 26.9% | 30.5% | 24.4% |

| National | 21.8% | 26.5% | 22.8% |

Methodology

This report is based on a Redfin analysis that uses MLS listing data and county-level median household income by veteran status from IPUMS microdata, aggregated to the county level for metro and national analysis. A person is considered a veteran if they were on active duty in the U.S. military in the past, but not now. For two metros in our top 50, where IPUMS does not publish county identifiers (Denver and Miami), we used metro-level IPUMS data to impute county values.

The analysis measures the share of active listings, i.e. homes that were for sale at any point between January and September of each year that were affordable to veteran and non-veteran households, nationwide and for the 50 most populous U.S. metro areas.

A home is considered affordable if the estimated monthly mortgage payment is no more than 30% of the group’s median monthly income. Monthly payments include mortgage principal and interest, property taxes, insurance, and PMI.

Loan assumptions:

- Veteran (VA loan): 0% down, 2.15% VA funding fee, no PMI, Mortgage News Daily VA 30-year rate.

- Veteran (Conventional loan): 15% down, 0.3% annual PMI, Freddie Mac PMMS 30-year fixed rate.

- Non-veteran (Conventional loan): 15% down, 0.3% annual PMI, Freddie Mac PMMS 30-year fixed rate.