(Oil & Gas 360) – Springtime Seasonal-Low Territory For Natural Gas Makes Next Extra-Good, Buy-Low Opportunity With Supply/Demand Trends Consensus Beating.

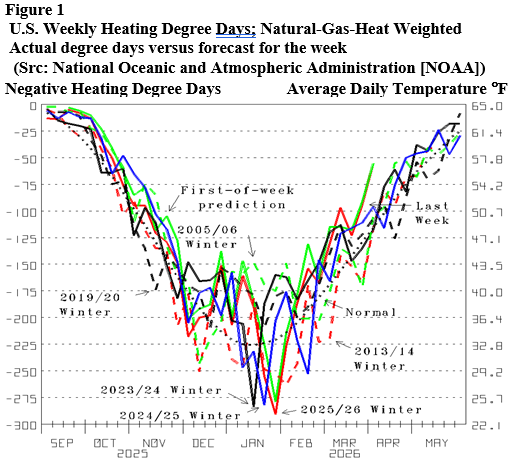

The Winter Delightfully mild has consensus interest, desires and expectations, on supplying natural gas and its prices, low. Only 5 of the 28 weeks since mid-September (Figure 1, red line), weighted for natural gas heat colder than normal (bold dot) highlights Winter 2025/26 another delightfully mild one. And yesterday’s forecast for this week (green line) predicts a temperature that is normal for the beginning of May. The temperature since November has averaged 2.0 °F warmer than normal and 0.4 °F warmer than last year (blue line).

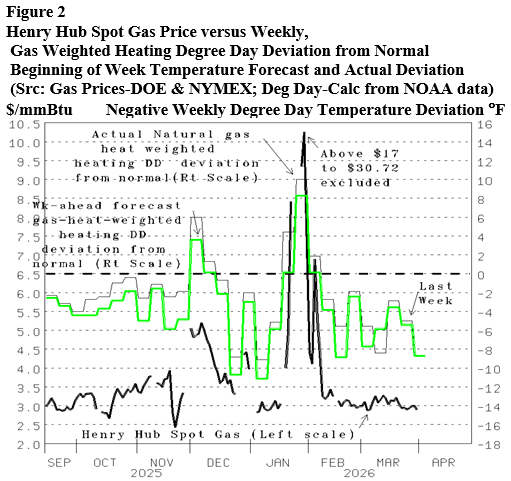

Late January into February notably cold tugged the Henry Hub price up to $30.72. Delightfully mild since has it back where it was when January began. 291 natural gas heat weighted degree days experienced the last week of January (Figure 2, line, right scale) was 10 °F colder than normal (bold dash, right scale). A record 360 Bcf was needed from inventory to meet the load. A new weekly withdrawal record. It tugged the Henry Hub spot price of natural gas up to $30.72 per mmBtu January 26th, $17.19 the 27th, $9.34 the 28th and $10.25 the 29th (bold line, left scale). The prices and withdrawal would have been higher were the coldest temperatures not centered on a weekend. However, temperatures averaging 4.6 °F warmer than normal since has the price back down below $3.

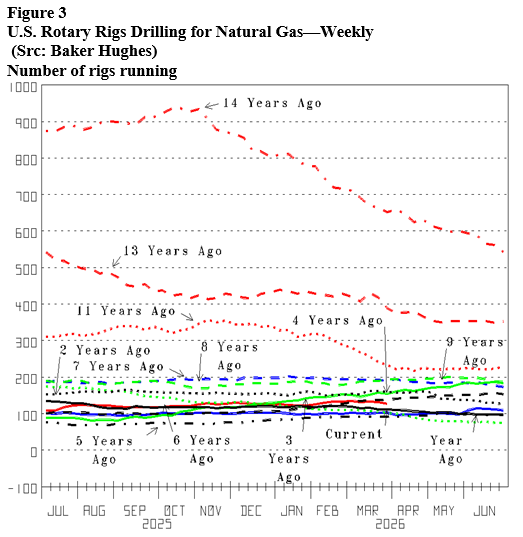

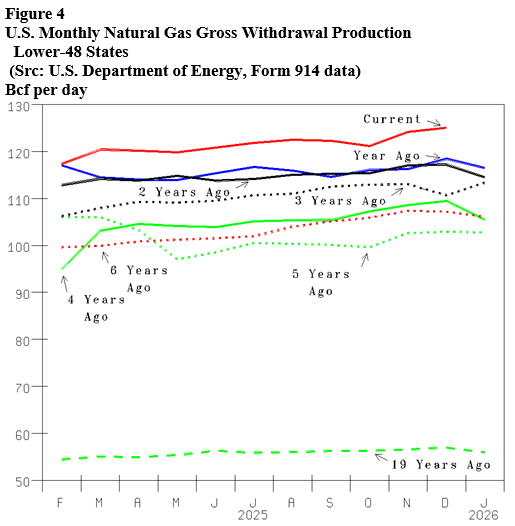

Low natural gas price expectations and investing disinterest is helped by the sense there is plenty of supply, helped by 23% more rigs drilling for natural gas now than last year. The Fracking Revolution, working wonderfully for natural gas had over 900 rigs drilling for gas in the Fall of 2011 (Figure 3, bold red, dot-dash). The Coronavirus Recession deflating had only 68 drilling that Summer (bold, dot-dot dash). UP to 103 last year (blue line) restored production growth (Figure 4) and 127 last week (red line) is a 24 (23%) year-over-year (YOY) increase.

Rigs drilling for natural gas declining to 68 during the Coronavirus Recession had lower-48-state production decline 6.295 Bcf/d YOY. 127 drilling now has production up 6.662 Bcf/d (5.6%) YOY. Activity dropping and natural gas prices briefly negative with the Coronavirus Recession dropped the number of rigs drilling for natural gas to a 68 low in the Summer of 2020 (Figure 3). That reduced lower-48-state natural gas production to 99.596 Bcf per day (Bcf/d, Figure 4, green dot) in October of 2020, down 6.295 from 105.891 in 2019. Rigs drilling for natural gas increasing from 103 at the end of March last year to 124 last August, 130 in December and 127 now (Figure 3) has production up to another new 125.114 Bcf/d record high in December (red line), up 6.662 (5.6%) YOY.

Temperatures mild, solar and wind electricity generation gains plus coal gains have natural gas demand showing little YOY growth. Last Winter colder had natural gas demand show good YOY increase December through February (Figure 5, blue line versus bold line). However, since then demand shows little YOY increase (including red versus blue). Except for the three cold weeks January into February.

By oilandgas360.com contributor Michael Smolinksi with Energy Directions

The views expressed in this article are solely those of the author and do not necessarily reflect the opinions of Oil & Gas 360. Please consult with a professional before making any decisions based on the information provided here. The information presented in this article is not intended as financial advice. Contact Energy Directions for the full report. Please conduct your own research before making any investment decisions.