- The share of homeowners who are “in the money” for a refinance has hit its highest level in over four years as mortgage rates dip to around 6%.

- But less than 1 in 10 eligible homeowners have refinanced, even though they stand to save money.

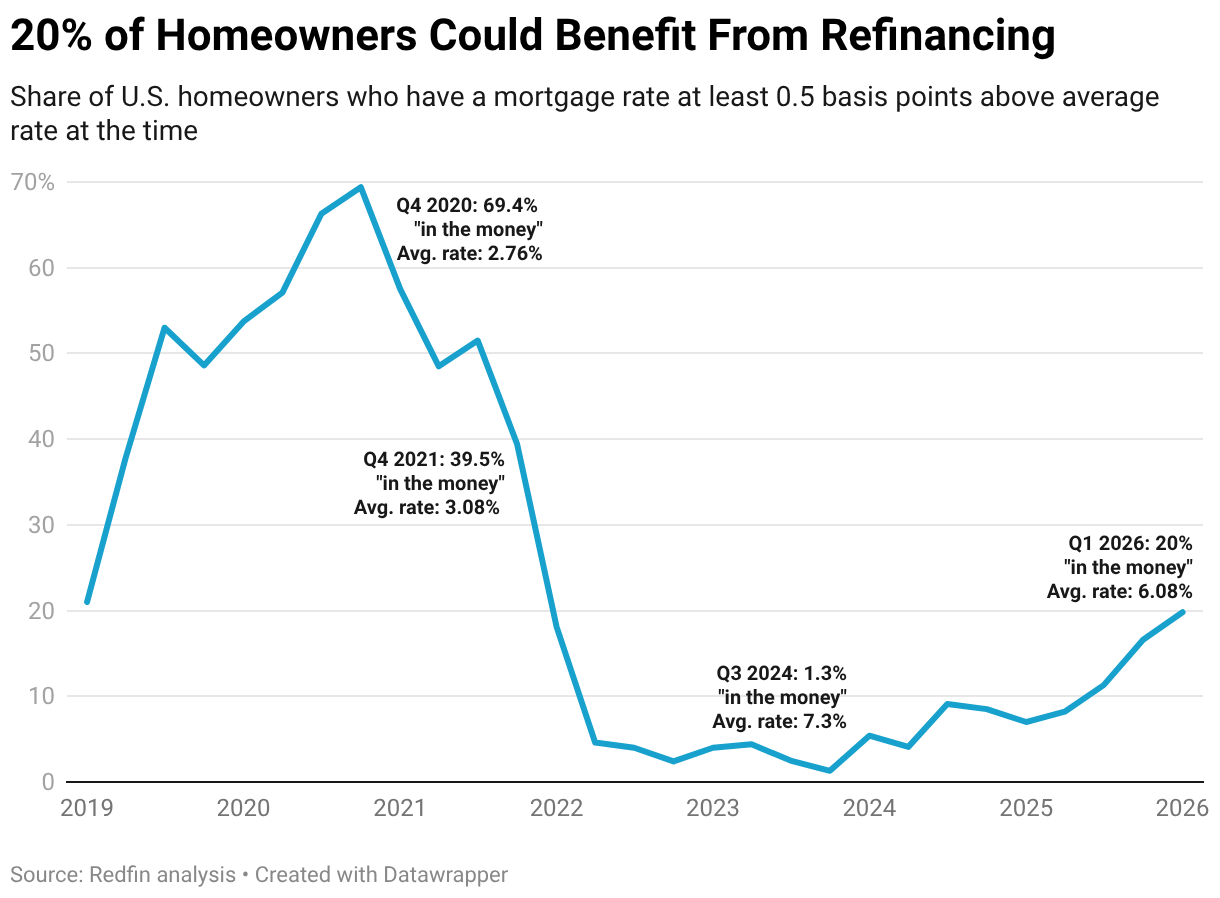

One in five (19.8%) U.S. homeowners with a mortgage could save money by refinancing to a lower rate, the highest share in over four years and up from just 7% a year ago.

That’s based on a 6.08% mortgage rate, the average so far this year. A homeowner is “in the money”–meaning they could save money by refinancing–if their current mortgage rate is at least 50 basis points above the prevailing mortgage rate; for instance, if they have a 6.5% mortgage rate and the prevailing rate is 6%.

This is according to a Redfin analysis of homeowners who could benefit from refinancing because current mortgage rates are lower than the rate on their existing loan. Throughout this report, when we refer to the share of “homeowners” who are in the money for a refinance, we mean the share of U.S. mortgage debt that is in the money to refinance. The portion of those loans that were actually refinanced (i.e. the take-up rate) is also a portion of all “in-the-money” U.S. mortgage debt. The current refinance take-up rate covers the first quarter of 2026, using an extrapolated estimation. Please see the end of this report for more on methodology.

There are two main reasons more homeowners are in the money for a refinance this year:

- Mortgage rates dropped down to 6% in February and early March, the lowest level in three and a half years.

- Mortgage rates were elevated above 6% for so long that 21.2% of U.S. homeowners had a rate above 6% as of the third quarter of 2025, the highest share in a decade. That marks the first time in five years more borrowers have a rate above 6% than below 3%.

Say someone bought a $500,000 home in October 2023, when rates hit a 20-year high of 7.8%. Their monthly mortgage payment would be about $3,700, assuming a 20% down payment. Refinancing to a 6% rate would bring the payment down to about $3,200, saving $500 per month. If the homeowner pays $10,000 in refinance fees, it would take less than two years–20 months–for the monthly savings to pay for the fees.

The last time this many homeowners were in the money for a refinance was the end of 2021, when mortgage rates averaged 3.08% and roughly two in five (39.4%) would have benefited from refinancing. The in-the-money share peaked at nearly 70% at the end of 2020, when mortgage rates plummeted to 2.76% during the pandemic.

Despite Potential Savings, Just 9% of Eligible Borrowers Have Refinanced

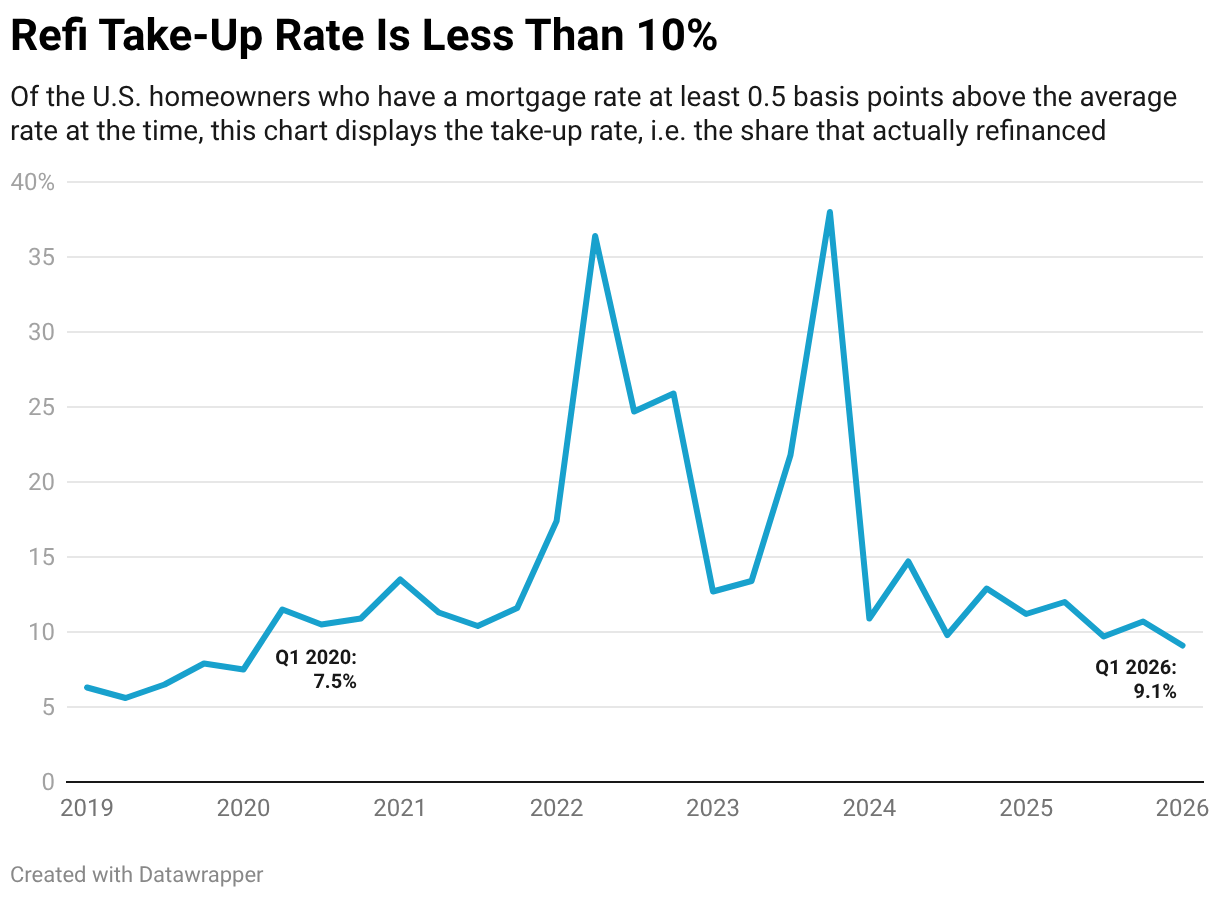

Just 9.1% of homeowners who could save money by refinancing to today’s average rate (6.08%) have actually done so, as of the first quarter of this year. That’s the lowest “take-up rate” for homeowners who could benefit from refinancing since the beginning of 2020.

Zooming out to all mortgaged homeowners in the U.S., 1.8% have refinanced so far in the first quarter.

“For homeowners who are in the money, refinancing now could meaningfully lower monthly payments and total interest costs over the life of the home loan,” said Bill Banfield, chief business officer at Rocket. “Even a modest rate reduction can add up to big savings, helping free up cash, build equity faster, or better weather future financial uncertainty. Homeowners may also consider whether refinancing could have advantages other than putting money back in their pocketbooks every month. For instance, they could consider consolidating debt or changing their loan type. Some people take advantage of lower rates to change the length of their loan and pay it off faster while keeping essentially the same monthly payment.”

While refinancing to a lower rate could save money in the long run for many homeowners, there are several reasons so few people are actually doing it:

- Waiting for lower rates. Mortgage rates can shift quickly; people may be hesitant to lock in a rate if they think rates will dip further in the near future, even if they could save money now. But homeowners should also consider that rates could go back up, and that they can refinance again if rates fall significantly more.

- Limited awareness. Not all borrowers regularly review mortgage options; many may simply be unaware they could save. Homeowners can save money by paying attention to changes in mortgage rates.

- Closing costs and fees. While refinancing costs can seem large on paper, many homeowners will be able to pay them off quickly with the amount they’re saving on interest every month.

When mortgage rates were sitting at record lows during the pandemic, dipping below 3% for much of 2020 and 2021, the take-up rate hovered around 1 in 10 eligible borrowers per quarter. The take-up rate peaked at 13.5% in the first quarter of 2021, when the average rate was 2.88%.

Today’s take-up rate is similar to what it was during each individual quarter of 2020 and 2021. But looking at those eight quarters together, more than half of in-the-money borrowers refinanced during that time.

It’s also worth noting that the take-up rate jumped to 38% in the fourth quarter of 2023, when rates were at a two-decade high. That’s because just 1.3% of homeowners were in the money for a refi; the actual number of homeowners who refinanced is much lower than the 38% suggests.

Homeowners Left Massive Amounts of Potential Savings Untapped

Americans refinanced an estimated $223 billion worth of home loans in the first quarter.

But they could have refinanced $2.24 trillion worth of home loans. That $2.24 trillion represents the total loan value of the 90.9% of in-the-money homeowners who didn’t refinance.

Methodology

This is from a Redfin analysis of homeowners who could benefit from refinancing because current mortgage rates are lower than the rate on their existing loan. Throughout this report, when we refer to the share of “homeowners” who are in the money for a refinance, we mean the share of U.S. mortgage debt that is in the money to refinance. The portion of those loans that were actually refinanced (i.e. the take-up rate) is also a portion of all in-the-money U.S. mortgage debt. Rate distribution and unpaid mortgage balance data is as of the third quarter of 2025, the most recent data available, while values for the fourth quarter of 2025 and the first quarter of 2026 are derived using linear extrapolation based on the trend from Q4 2023-Q3 2025. Refinance volume data is available through the fourth quarter of 2025; refinance volume for the first quarter of 2026 is from a Fannie Mae housing forecast.

Mortgage-rate data is based on average 30-year fixed mortgage rates from Federal Reserve economic data. Mortgage-rate distribution and total unpaid mortgage balance data is from the Federal Housing Financing Agency’s National Mortgage Database.

The percentage of mortgages that are in the money is calculated using a uniform distribution assumption within each rate bucket. The mortgage rate distribution data provides five buckets: 6.0% – 8.0%, 5.0% – 5.9%, 4.0% – 4.9%, 3.0% – 3.9%, and 2.5% – 2.9%. To calculate the in-the-money percentage, we: 1) Determine the threshold rate (30-year rate + 0.5%), and 2) Identify which rate buckets are entirely above, entirely below, or partially intersect the threshold. For buckets entirely above the threshold, we added 100% of mortgages in that bucket to the in-the-money total. For buckets partially intersecting, we used uniform distribution to calculate the proportion above the threshold. Buckets entirely below are excluded from the calculation.