Link to Report: Macro Volatility Digest

WHAT STANDS OUT:

- Oil 1M implied volatility jumped almost 40 pts last week to a high of 104% – highest since 2020 (when oil prices went negative) and trading near the peak volatility we saw during the 2008 GFC. What’s even more notable is the widening volatility risk premium, with implied vol trading at almost double the level of realized volatility, suggesting fears of further escalation in this crisis. Oil volatility risk premium is currently at its highest level on record, going back 20 years.

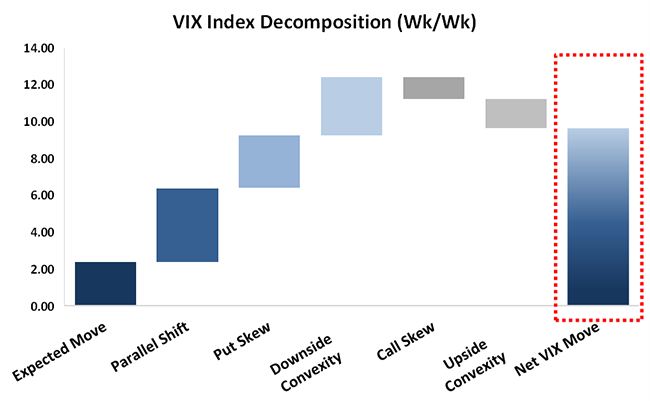

- Equity volatility jumped higher last week, with the weak US jobs number adding fuel to the stagflation worries. The VIX® index gained almost 10 pts to 29%, far outpacing the move in SPX® realized vol (1M realized vol +0.5 pt). Given the relatively modest SPX index decline of -2% last week, the “expected” VIX index increase was only +2.4 pts. Instead, the VIX index jumped 4x that. The outsized increase in the VIX index was a combination of higher bid for optionality reflecting the increased macro and geopolitical uncertainty (contributing +4.0 pts to the VIX index), as well as a notable increase in hedging demand going into the weekend, with investors selling calls to fund downside protection (contributing +3.3 pts). See chart below. For more on our VIX index decomposition model, see link to full paper here and web portal here.

- Globally, Emerging Markets and Europe led the increase in equity vol, with those regions more vulnerable to the energy shock. Both EFA and EEM 1M implied vol jumped over 11 pts last week. The EEM-SPX 1M implied volatility spread doubled wk/wk to a 15-year high of 14.6%.

Chart: Drivers of the VIX Index Increase Last Week

Source: Cboe