By David Enna, Tipswatch.com

Auctions for new 5-year Treasury Inflation-Protected Securities happen twice a year, in April and October. Because of the relatively short term, and the different inflationary conditions leading up to each maturity date, the 5-year TIPS auction is hard to predict.

I got caught by this phenomenon in October 2023, when a new 5-year TIPS (CUSIP 91282CJH5) auctioned with a real yield of 2.440%, well below the “market” yield of about 2.55% or higher. I was surprised. But I shouldn’t have been.

I wrote about this in an Oct. 20, 2023, article with the subtitle “There is an explanation for everything, right?” The basic lessons are these: 1) The October TIPS auction will get a real yield less than the apparent market rate, and 2) The April TIPS auction will get a real yield higher than market.

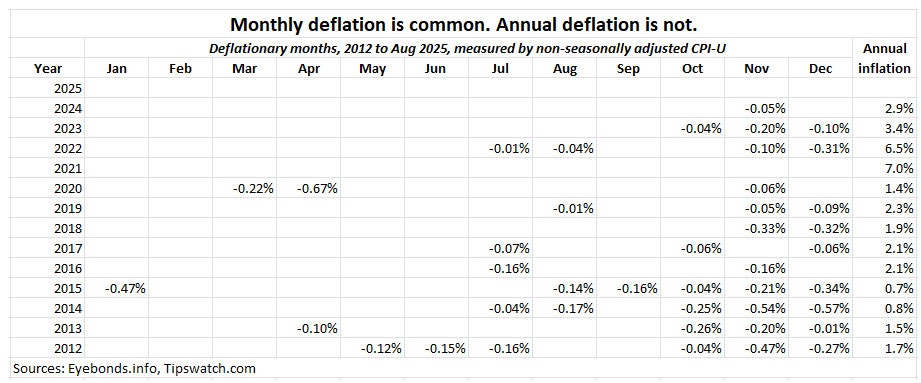

The reason is a bit esoteric: Non-seasonally adjusted inflation has a strong seasonal pattern, generally running higher than headline CPI from January to June and lower from July to December. The closing value of the April TIPS (reflecting inflation through mid-February) is much more likely to be exposed to end-of-the-year deflation, and therefore the April TIPS gets a higher real yield than “market.”

I created a chart last year to prove the point — the April 5-year TIPS gets a higher real yield than the October version:

Also see: ‘Inflation Guy’ explains seasonal adjustment (or lack thereof)

Here’s another chart that shows how deflationary months are quite common in the last three months of the year, which would reduce the maturing value of an April-issued TIPS:

What does this all mean?

On Thursday, Treasury will auction $26 billion in a new 5-year TIPS (CUSIP 91282CPH8). That will be the largest auction-size ever for this term, up from $25 billion in April and $24 billion in October 2024.

You can track the real yield of the April TIPS in real time on Bloomberg’s Current Yields page, which shows a Friday closing real yield of 1.23%. The U.S. Treasury also provides a daily estimate of the real yield of a full-term 5-year TIPS, which closed Friday at 1.30%.

Saturday morning, Vanguard’s bond-trading site was showing an “indicative yield” of 1.235% for the upcoming auction, obviously based on current trading in the April TIPS.

Conclusion: All of these indicators are wrong. At this point in time (things will change by Thursday) I’d predict this TIPS would get a real yield of 1.15% or lower. Past results show us the real yield will be lower than the 1.23% “market” created by the April TIPS. In other words, be prepared to be surprised.

Definition: The “real yield to maturity” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 1.15% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 1.15% for 5 years.

Real yields will rise and fall next week in the days leading up to the auction. But it will be interesting to see how close this 5-year TIPS gets to the 1.10% fixed rate on the current Series I Savings Bond, available through the end of this month.

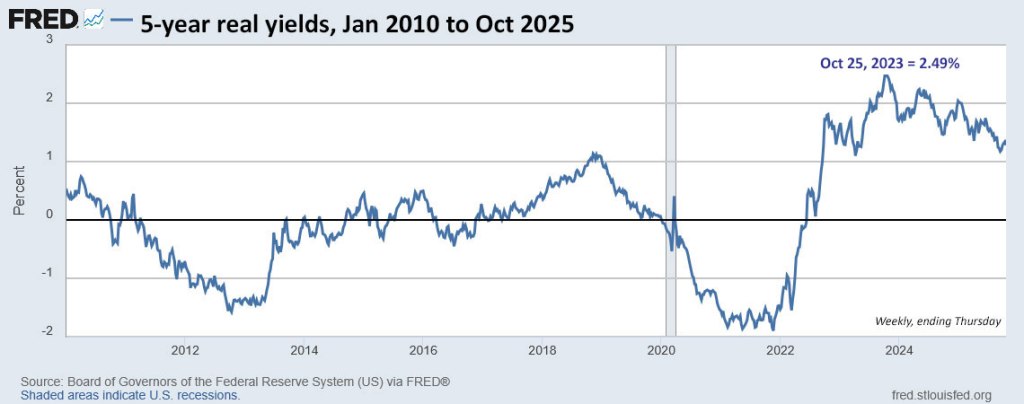

Here is the trend in the 5-year real yield over the last 15 years:

Side note: Remember that 5-year TIPS auction of Oct. 19, 2023, when the real yield was a “disappointing” 2.440%? Turns out that the auction came within a whisker of the 15-year high real yield of 2.49%, set a few days later.

Pricing

Because this is a new TIPS, the coupon rate will be set to the 1/8th percentage point below the auctioned real yield. That means the TIPS will have an unadjusted price slightly below par value. It will carry a minimal inflation index of 1.00148 on the settlement date of Oct. 31. The end result will be a price slightly below par. In other words, a $10,000 investment in this TIPS should cost very close to $10,000.

Inflation breakeven rate

Using the U.S. Treasury estimates of 1.30% for a five-year TIPS (probably too high) and 3.59% for a 5-year Treasury note (probably accurate) you get an inflation breakeven rate of 2.29%, a bit below recent trends. If you adjust the likely yield to 1.15% the breakeven rate rises to 2.44%, higher than recent trends. My conclusion: Who knows?

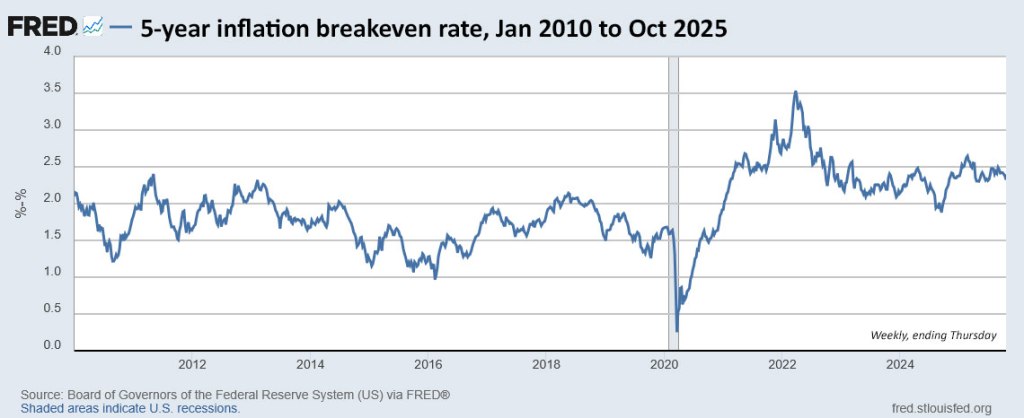

Here is the trend in the 5-year inflation breakeven rate over the last 15 years:

Thoughts

I often note that the 5-year TIPS is most sensitive to the Fed’s short-term rate cuts, and that has proven accurate in 2025. The 5-year real yield has fallen about 67 basis points since January 1, compared to 48 for the 10-year and only 8 for the 30 year.

Is a real yield around 1.15% to 1.20% still attractive for a 5-year TIPS? Yes, but it depends on your investment needs. As the yield approaches the now-current 1.10% fixed rate on the I Bond, the savings bond becomes more attractive, given its tax-deferral, deflation protection and flexible maturity. (The I Bond’s fixed rate is likely to fall to 0.9% at the November 1 reset, but 1.10% is available through the month of October.)

I suspect their won’t be much demand for this auction from small-scale investors. If you are jumping aboard, let me know your thoughts in the comments section.

This TIPS auction closes Thursday at 1 p.m. ET. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

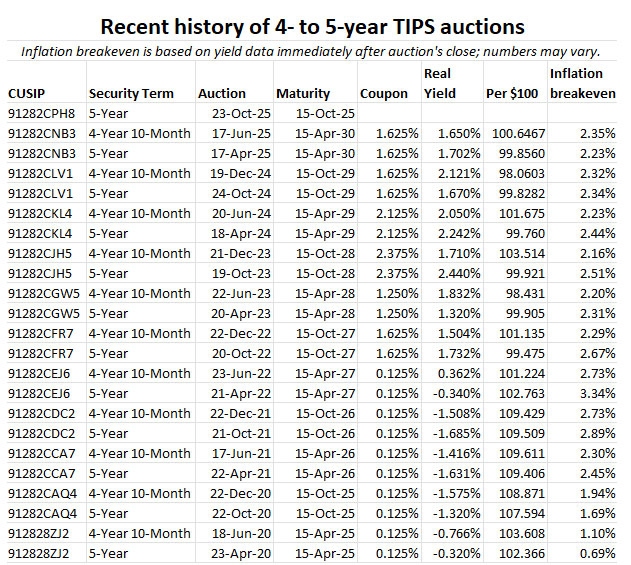

I will be posting the auction results soon after the close on Thursday. Here is a history of auction results for this term over the last 5 years:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.