Mandy Xu

▬

October 13, 2025

Link to Report: Macro Volatility Digest

WHAT STANDS OUT:

- US option volumes broke records on Friday after US-China trade tensions re-ignited, with over 108M contracts trading across products. SPX® options also set a new record, with 6.4M contracts trading (exceeding the previous high of 6.0M set on April 4th), with 0DTE options making up 60% share. VIX® options surged as well, with volumes running 3x its 20-day average.

- Despite the record activity, there was little panic in the market, as seen by VIX index levels that remain fairly pedestrian by historical standards. The increase in implied volatility also trailed the jump in realized vol – as a result, the volatility risk premium actually fell last week. There was also little demand for left-tail hedges, though demand for right-tail upside exposure increased, similar to what happened in April as investors positioned for a potential softening in trade rhetoric.

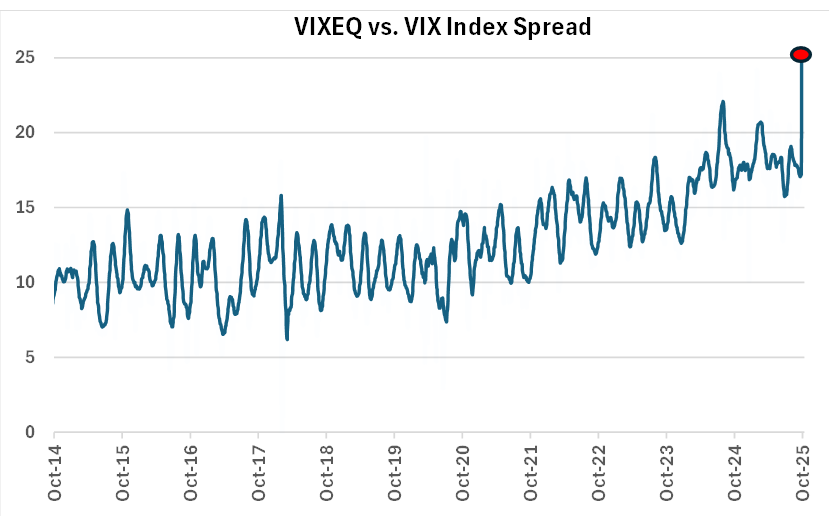

- With earnings kicking off this week, what stands out is the continued bid to single stock vol, with the VIXEQSM index up another 6.6 pts last week. The spread between single stock vol versus index vol, as measured by the VIXEQ-VIX index spread, widened to a new record high of 24.7% (see chart below). Not surprisingly, most of the increase in dispersion have come from the large-cap Tech names as investors look to earnings to justify their valuation.

Chart: Single Stock Vol at Record High vs. Index

Source: Cboe